“Money is Equity”

It’s a tale as old as currency: more money creates inflation. The idea was formalized in 1962 by Nobel-prize winning economist Milton Friedman in Capitalism and Freedom:

“Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.”

A more recent understanding of money frames it as a force that frees nations from budgeting constraints. Effectively, the ability to print money grants them a bottomless wallet, and all the fuss about debt and taxation is mainly a way to control inflation. This is is the core thesis of Modern Monetary Theory (MMT).

Haizhou Huang and Patrick Bolton’s book, Money Capital, reacts to these ideas with a new angle: money is equity. Much like a company issuing shares to finance value-creating investments, a country can issue money for various strategic reasons, whether it is to save failing banks, pay back debts, finance infrastructure projects, or take advantage of inefficient exchange rates. And much like shares don’t necessarily depreciate during a stock issuance, neither should money when it is doled out en masse. The authors argue that as long as money is dedicated towards investments that boost the economy and increase productivity, its value need not be affected.

The notion that money is akin to equity has fascinating implications, not least of which is the suggestion that tried and true lessons from the corporate world around how to structure capital might also apply to nations. This key point is why Charles Goodhart himself describes the book as “important for all those interested in monetary issues to read and learn.”

So if you’re a crypto aficionado, a policy geek, a finance nerd, or you’re just curious about how money works, read on!

Disclaimer

Before diving further into the undeniably radical, breath-taking, and revolutionary ideas this book introduces, it’s worth noting that one of the book’s authors is my father. Since Scott Alexander does not know me, and since this deanonymizing fact obviously affects my impartiality in reviewing the book, it feels only right for me to share it.

It’s also worth sharing that I’m by no means a macroeconomist. When I tried to study the subject in college, my parents (both economists) told me not to waste my time on cursory introductions to the field. The end result, and a big regret of mine, is that I’ve barely scratched the surface on the very subject responsible for my parents’ first meeting.

To rectify that, I decided that reading Money Capital in the detail required to write a passable review would be a fun challenge. And boy oh boy, did I bite off more than I could chew: the book is definitely not a layperson’s book. But don’t let that deter you, fellow reader! In this brave new era of chatbots and increasingly online academics, the answers to your deepest questions are often just a query or an at-mention away. This book review, indeed, would not have been possible without ChatGPT and the kind patience of my Dad.

I hope this can also serve as an invitation for others to read ambitiously and reach a little too far beyond their expertise: it’s deeply rewarding and surprisingly feasible in this day and age.

A Fateful Cab Ride

The book opens with a scene I’ve since heard about at the dinner table many times. It was one of those magical cab rides through a glittering city; a moment of zen shared between old friends, driving from one exciting commitment to another. The kind of momentary pause that can spark great ideas.

As my father and his co-author rode through a bustling Tiananmen Square, the centerpoint of a modern city once dominated by swarms of bicycles and rickshaws, perhaps there was a sense of mystique in the air created by how the Chinese economic miracle came to be. I certainly felt it when I first traveled to Beijing with my Dad in 2008, and saw a city that made my hometown of New York feel small.

As two respected economists, the pair already knew the full story of China’s incredible, unprecedented, record-breaking 40 years of economic growth. But that didn’t answer the fundamental “How?” of it. How had China made it look so easy? It was in the taxi that an answer came.

How did China Finance Its Growth?

That is the question posed in Chapter 4 of the book. In 1978, China was one of world’s poorest nations. Its GDP per capita barely reached RMB423, or US$270 in 1979. By 2019, its GDP per capita was RMB70,890 or US$10,427, a 166 fold increase, or 37 fold in US dollar value. The nation’s GDP went from RMB410 billion to RMB98.7 trillion, a 54 fold increase in equivalent US dollar terms. Meanwhile, the world’s GDP only increased 7.7 times in US dollar terms, from 10.1 trillion to 87.7 trillion. In the authors’ words:

“There is no other example in history of such rapid and sustained economic growth, which is all the more remarkable given that China had the largest population in the world. This was not an example of a small city-state that sees its economy prosper through trade and agglomeration externalities, but the lifting out of poverty of over 20 percent of the world’s population.”

The authors build on the ideas they introduce in the book’s first three chapters to tell a story in two parts: how China gradually built the financial capacity required to finance large-scale investments, and how it originated those investments at such a large scale and for so long.

Building Financial Capacity

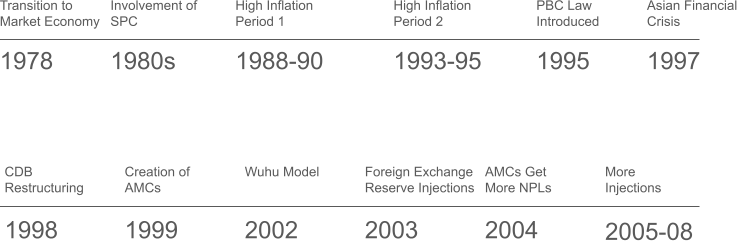

The chapter on China, like many of the book’s chapters, dives into a detailed historical account of important macroeconomic developments, which I found helpful to plot on a timeline:

The authors highlight the following events in China’s journey towards strengthening its banks’ credit:

1978: When Deng Xiaoping took power, China’s centrally planned economy was crumbling, with many of its state-owned enterprises (SOEs) at risk of collapse. He initiated the nation’s transition to a market economy.

1980s – Early 1990s: The State Planning Commission, mostly concerned with supporting people’s livelihoods, remained the central authority dictating how funds were allocated. During this time, state-owned enterprises began to retain a greater share of their profits. In addition, amidst the uncertainty of the economic paradigm shift and with no guaranteed social security, Chinese families began to save – a lot, which improved banks’ supply of credit.

1988-90 and 1993-95: China experienced periods of high inflation, as money flowed into SOEs even as their loss ratios increased. This ties into the authors’ central thesis that increases in money supply must be offset by positive net present value investments to avert inflation.

1995: The non-performing loan (NPL) ratio – essentially the percent of loans that are not being actively repaid – of the four largest Chinese banks reached a dangerously high 21.4 percent. The People’s Bank of China (PBC) officially moved away from commercial banking and had its mandate as a central bank enshrined into law, allowing it to take on its role as a supplier of money.

1997: The Asian Financial Crisis left China largely unscathed, since it did not have large foreign debt burdens and had more control over its capital account.

1998: Chen Yuan, in charge of the China Development Bank (CDB), instilled financial responsibility, hiring well-trained loan officers and implementing rigorous due diligence processes, ensuring that loans are issued to finance value-enhancing investments,. Meanwhile, the Ministry of Finance (MOF) injects RMB270 billion into the four major Chinese commercial banks.

1999: Four Chinese Asset Management Companies (AMCs) took over RMB1.4 trillion in NPLs, backed by loans from the MOF, the PBC, and commercial banks.

2003: Thanks to historically cheap exports and capital control, China had accumulated large foreign capital reserves. The PBC creates the Central Huijin Company, later a key component of China’s sovereign wealth fund. Using some clever accounting, The Central Huijin injects capital into Chinese banks, reflected as an increase in equity investments in the banks, a decrease in foreign exchange reserves, and an increase in deposits held by money banks.

2004: AMCs took on an additional RMB1.6 trillion in NPLs.

2005 and 2008: The PBC and the Central Huijin injected further foreign exchange reserves. In total, these injections added up to RMB626 billion. As of 2021, the market value of these stakes was RMB2.24 trillion, a 283 percent return on investment.

In sum, by swapping debt for equity, China was able to gradually resolve its unpaid loan problem. This extensive cleanup and recapitalization helped its banks extend more credit to sustain its economic growth. In particular, China relied on its strong banking system to weather the 2008 financial crisis with a massive economic stimulus, seeing a low of 6.4 percent growth in the first quarter of 2009, which rebounded to 10.6 and 11.9 percent in the third and fourth quarters.

Originating Value-Enhancing Investments

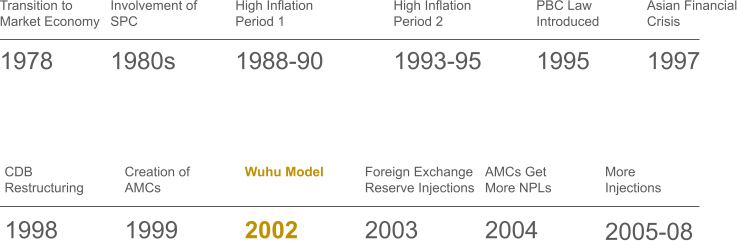

That all sounds well and good, but macroeconomists will tell you that that’s still not enough to sustainably finance growth and construction, whose returns are notoriously too low and too far into the future. This is where, per the authors, the last piece of the puzzle comes in: the legendary Wuhu Model.

In 2002, the Anhui provincial government created a structured financial contract among four lenders: the CDB, the Wuhu municipal government, private-sector developers, and the Anhui provincial government itself, in order to finance highway construction, water supply improvements, landfill construction, and other projects. This four-agent long-term relation improved on the typical bilateral principle-agent relation between a public investment bank and a local government borrower that is customary in public infrastructure works.

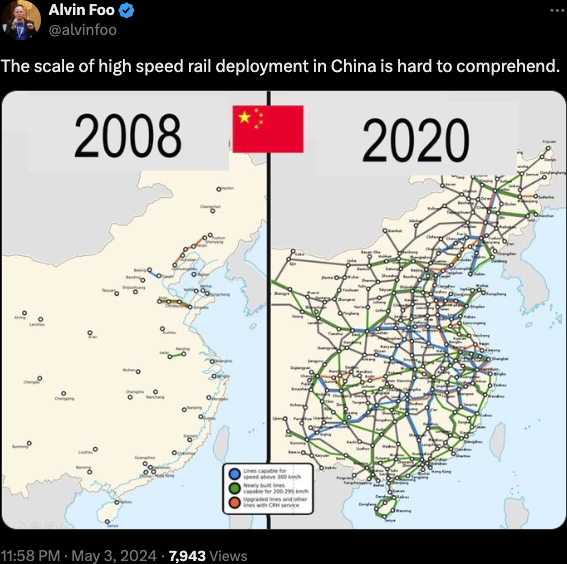

Perhaps the most innovative centerpiece of the contract was how land value appreciation was captured. Essentially, the PBC guaranteed that its loan to private developers would be repaid by collateralizing development rights, which would appreciate in value as the land was improved through ongoing investment. In conjunction with subsidies pledged by the city of Wuhu in the event that construction companies could not repay their loans, this meant investment in the project was significantly de-risked for Chinese banks. This model provided the CDB with a powerful framework that it was able to re-apply throughout the nation, which partially explains this incredible picture:

Side note: if you’ve ever had the privilege of taking the subway in Hong Kong, you will know how powerful the capture of land value appreciation can be. Not only is it one of the cheapest and most modern subway systems in the world, it is the only profitable system in the world. The Hong Kong Transport Department pulled off this remarkable feat through a scheme that granted them exclusive development rights near subway stations.

Compare this to how New York approached the development of Hudson Yards, for which the Metro Transit Authority (MTA) financed an expensive extension of the 7 line. Over the course of the project, what was once an abandoned railyard was transformed into an entire city neighborhood with over a dozen new towers containing plenty of luxury housing – a tremendous increase in land value. Now, how critical was the subway extension to that appreciation in land value? As most New Yorkers can attest, subway access is everything, so it certainly played no small part. But how much of that massive appreciation in land value was used to finance the subway extension? Zilch. Instead, it was funded by an expected increase in future citywide tax revenues, which kind of feels like the MTA got scammed.

Returning to China, the end result of all this economic activity was the creation of a positive feedback loop, as the high growth rate of the Chinese economy boosted the performance of its banks, which in turn were able to finance more growth. At the core of all this was the strength of the CDB, which went beyond cheap financing: as part of the Wuhu Model, it originated infrastructure investments, which it helped coordinate with local governments and municipalities through long-term, coordinated plans that ensured repayment of debt through a new value capture model that relied on appreciation of land values in urban areas.

The China story is central to the authors’ thesis, as it highlights the biggest issue with the unlimited credit creation that MMT attributes to nations. Funding without concern for asset quality, as shown early on in China’s economic turnaround, only leads to inflation, similar to how a company issuing shares without creating new value will dilute its stock price. Instead, it is the discipline shown by the CDB in forging good contracts and pursuing value-creating investments that allowed China to dramatically expand its money supply without inflation.

Effective Capital Stucture of Nations

You can imagine the effect such lofty tales of economic miracles had on me growing up. Even though I never fully understood their underpinnings, I was inspired by the conceptual frameworks my parents studied, which seemed to carry the potential to improve the lives of millions. The belief that the right analytical perspective can massively increase the good in the world is probably what primed me to become the unapologetic fan of effective altruism that I am today.

My father and his colleague’s thesis, when applied to China, shows that a simple idea like the strategic deployment of money has the capacity lift a nation of over a billion inhabitants out of poverty. But could their line of thinking apply to other nations?

During the years they worked together on the book, I had the opportunity to hear firsthand from the authors that the answer was an unequivocal yes. Over the course of many dinners I was lucky to share with them over the past decade, I heard them wax poetic about economic shifts the world was experiencing, each of which seemed to validate their theories. They were onto something!

The European Sovereign Debt Crisis

Among many such stories, I heard about the impossible situation Mario Draghi faced on July 26th, 2012. Europe’s widening sovereign debt crisis seemed to announce the impending and increasingly inevitable abandonment of the Euro. On that day, he was set to talk to a room full of financial executives, policymakers, and leaders of nations. What could he possibly say to avert the crisis? Was the end of the Euro to be the legacy of the third president of the European Central Bank, only one year into his term?

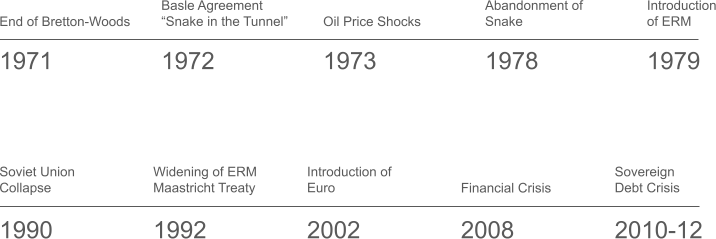

History of the Eurozone

In the book, the authors provide a thorough account of the events leading up to that day, presented on the timeline below:

Here’s what all this meant, in more detail:

1971: Facing mounting inflation, costly wars abroad (most notably the Vietnam War), and increasing foreign exchange pressures, President Nixon announced that the U.S. would no longer convert dollars to gold a a fixed value, effectively ending the Bretton-Woods System. This move led to the current system of floating exchange rates that we see today among major currencies.

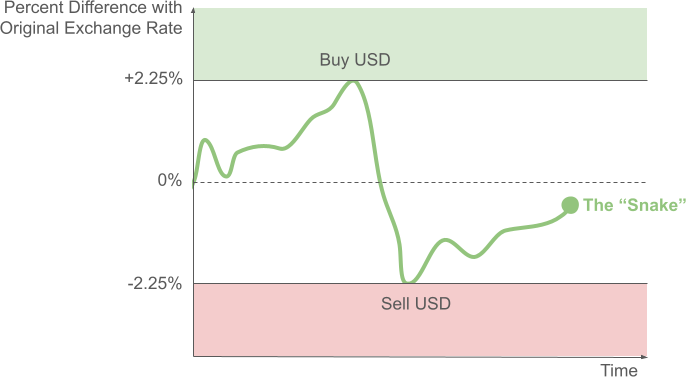

1972: As a way to maintain stability in their exchange rates, European nations agreed to keep their currencies within a narrow band of values relative to a starting exchange rate with the US dollar, by buying and selling domestic currency if its exchange rate got too high or too low:

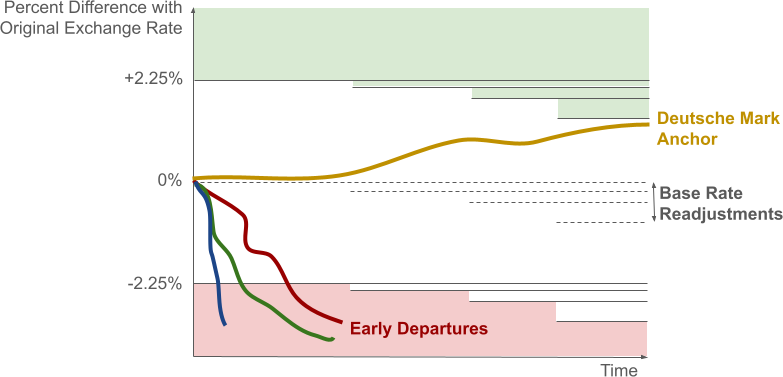

Unsurprisingly, this perhaps overly simplistic system rapidly ran into issues, and in practice played out more like this:

The UK’s Pound Sterling, Irish Punt, and Danish kroner had to exit the system in short succession due to speculative attacks. The base rate had to undergo frequent readjustments to keep the system sustainable. And the strength of the German economy placed the Deutsche Mark as the de facto anchor of the snake, making it harder for other currencies to stay within the narrow band, placing pressure on those economies.

1973: Oil Price shocks caused France and Italy to seek to pay for the increased cost of oil imports by increasing their money supply, which led to multiple currency devaluations. During this period, the monetary snake failed to provide adequate exchange rate stability.

1978: The monetary snake was abandoned in favor of the Exchange Rate Mechanism (ERM), which had similar constraints, but did not require dependence on the US dollar.

1990: The collapse of the Soviet Union highlighted the weakness of the EMS by adding a layer of economic uncertainty and instability across Europe. German reunification led to substantial fiscal expenditures by Germany, creating inflationary pressures in Germany, which the German central bank responded to by raising interest rates.

1992: Many other countries followed suit. Indeed, money supply increases forestall recession, but also allow a country to gain temporary purchasing power when exchange rates are slow to adjust, as their currency might be overvalued. Therefore, other countries might want to seek to undo the effects of monetary growth in one country by also expanding their supply. This led to a strategic monetization game that eventually led Italy and United Kingdom to exit the ERM in 1992. Meanwhile, the Maastricht Treaty was signed, and the European Union was created, setting the stage for the monetary union to come.

2002: The new political conditions that followed the demise of the ERM led France to be willing to abandon its monetary sovereignty to keep up with Germany’s reunified economy, while Germany was willing to join a monetary union for which it could set the tone, with the European Central Bank headquartered in Frankfurt. The Euro was born.

Implications for Sovereignty

This period illustrates the importance of monetary sovereignty, thanks to which countries are able to control their response to economic recession, but also illustrates the weakness of a multi-currency system where slow-to-adjust exchange rates create incentives for competitive devaluation. In the book, the authors couldn’t help but offer a cheeky roast of cryptocurrencies, which have notoriously suffered from slow adjustment of exchange rates: “How could exchange rates of 19,000 digital currencies react immediately, especially in a bubbly environment?” write the authors. This is precisely what creates excess incentives to issue new cryptocurrencies and ride speculative bubbles.

Unfortunately, the newly created monetary union in Europe soon ran into the issues that an abandonment of monetary sovereignty implied.

2008: The Financial Crisis caused several European nations to face rising government deficits and debt levels. Greece, Ireland, Portugal, Spain, and Italy were particularly affected.

2010-12: As these countries’ debt levels rose, markets became increasingly fearful of the potential these nations would default, leading to higher borrowing costs and exacerbating their fiscal troubles. The European Central Bank offered bailouts, but with stringent austerity conditions that led to economic hardship. The disintegration of the Eurozone, so that these affected countries could regain monetary sovereignty, became a real possibility.

The Draghi Rule

Which brings us to Mario Draghi, who during his speech coolly delivered the line that would save the Euro: that the European Central Bank would do “whatever it takes” to end the crisis. In so doing, Mario Draghi presented the European Central Bank as an almost unconditional lender of last resort (LOLR), that is, it would guarantee the debt claims that were leading to the crisis. Soon thereafter, in September, the Outright Monetary Transactions (OMT) program was introduced, stating that the bank would make purchases of bonds issued by Eurozone member states under far more relaxed conditions. The combined effect of the speech and subsequent actions was to stabilize financial markets and lay the groundwork for economic stabilization of the Eurozone. Ultimately, the OMT never even had to be used.

Perhaps that story will remind some of Hank Paulson’s quote during the 2008 Financial Crisis: “If you've got a bazooka, and people know you've got it, you may not have to take it out,” which was in reference to the original LOLR rule, the Bagehot Rule: “to lend freely at a high rate against good collateral.” Indeed, the promise of such a backstop for solvent banks could avoid the risk of bank runs, as deposit holders knew their claims would be kept safe.

However, the authors of the book present Draghi’s attitude as more extreme than the Bagehot Rule, which states that emergency lending should be extended only to solvent banks. A more unconditional rule, which they nickname the “Draghi Rule,” could have interesting implications for banking crises, as during a financial crisis, it’s entirely possible that all banks would become insolvent, negating the effectiveness of the Bagehot Rule. The success of Draghi’s attitude in stabilizing the Eurozone indicates that having central banks adopt a more unconditional rule towards commercial banks could serve well in times of crisis.

What’s the Catch?

One might ask: what’s the point of even imposing conditions, if bank failures are so damaging to the economy? The Bagehot Rule, put forth by Walter Bagehot in 1873, came during a time when the gold standard limited central banks’ ability to act in times of crisis. For instance, in 1931, Danat-Bank in Germany experienced a significant bank run. The Reichsbank continued to lend to them until it hit the upper limit of the money issue that it could cover with its holdings in gold and foreign exchange, which in turn led to a universal bank run and a massive widening of the crisis.

Another catch is the moral hazard implicit in an unconditional backstop for banks: that it would encourage reckless lending for banks. As a result, the authors of the book propose a hybrid state-contingent rule, wherein the Bagehot rule is applied under normal circumstances, and the Draghi rule is applied in times of crisis. They notably show this to avert moral hazard by incentivizing banks to continue to screen for good entrepreneurs when choosing who to lend to (more on this later).

The question then arises: who determines when there is a crisis? A political question like this one would require a political process, which can be too slow to react to a crisis. Instead, the authors suggest the creation of an independent financial stability agency, working in parallel with the Federal Reserve, to decide what state the economy is in.

The 2008 Financial Crisis

I still remember the night Lehman Brothers went bankrupt, and the way my parents chattered in hushed voices about the dire implications of its insolvency. Indeed, it went on to mark the beginning of the international banking crisis that led to the Great Recession. Here too, hindsight tells us that providing a backstop to the company, in accordance with the Draghi Rule, could have averted the brunt of the crisis.

Nonetheless, many good lessons from past financial crises were applied: rather than fiscal and monetary tightening, the Federal Reserve initiated quantitative easing and lowered the federal funds rate to a minimum of 0-0.25 percent. As a result the Great Recession lasted only six quarters and saw a V-shaped rebound, a much better outcome than the Great Depression, which was handled via tax increases and higher interest rates.

Of particular interest to the authors of the book was the fact that the Federal Reserve made a substantial profit from its emergency lending to Citibank, Golmand Sachs, AIG, and others during the 2008-2009 financial crisis. Indeed, the effect of such an LOLR policy, in addition to stabilizing the economy, is to dilute debt claims through a massive increase in the money supply. The debt claims the Federal Reserve extended to banks were as a result relatively easy for banks to pay back, leaving the Fed with profits on the money that it lent at high interest rates.

The COVID Pandemic

Perhaps the most recent test of the authors’ thesis came in the form of the COVID Pandemic. The 2020 CARES Act injected a great deal of money into the economy without it being tied to value-increasing investments, which in the short run led to a lot of inflation. Perhaps the biggest surprise was how long the inflation lingered, which the authors argue came from a “cost push” due to supply chain issues and the rise in energy costs caused by the Ukraine conflict. This seems to be borne out by the fact that all nations experienced inflation, regardless of their fiscal and monetary response to the COVID financial crisis.

A Tale of Three Models

To support their historical analyses, the authors break up their detailed accounts of how nations financed investments, foreign currency reserves, and debt crises with a set of three macroeconomic models.

In their first model, the authors examine how financing interacts with inflation, and compare equity financing to debt financing under various economic conditions. In doing so, they first prove an equivalent version of the Modigliani-Miller theorem for nations, which for companies states that the capital structure has no impact on the valuation of the firm. The authors show that in the absence of information asymmetries, whether debt or equity is used for financing national investments only affects who receives the payoff: investors or creditors.

Then, they show how differences in beliefs about the monetary policy of a nation between residents and foreign investors does affect how the nation should elect to finance itself: if international investors belive the central bank will be more hawkish than a nation’s residents do, then the nation ought to issue domestic currency debt, which is why many countries barely rely on foreign-currency debt to fund their capital expenditures.

In their second model, the authors share how a hybrid Bagehot-Draghi rule LOLR strategy is desirable, and can even generate profits for the central bank. Furthermore, their analysis shows that banks are still better off spending resources to screen for good entrepreneurs to loan to in a hybrid framework, which nullifies concerns about the so-called “moral hazard” that banks will play fast and loose with their loans.

Last but not least, in their third model the authors show how international money neutrality breaks down when exchange rates do not instantaneously respond to changes in countries’ money supply, similar to the issues that arose under the EMS in Europe. They further show that a monetary union with fiscal transfers between nations is the most desirable way to money supply while averting sovereign debt crises.

These three models are at the core of the claims the authors support throughout the book with historical evidence. It’s worth checking it out the mathematics for yourself – without going into detail here, I found the models to be satisfyingly simple and elegant. An alternative to buying the book is to read the authors’ 2017 paper, which presents a lot of the proofs and assumptions underpinning the book’s macroeconomic models.

Final Thoughts

The book’s description of money as equity presents several actionable corollaries for nations and their central banks. Not least among these are the conclusions that optimal money supply depends on the quality of the investments the money will finance, and that a more extreme version of the Bagehot Rule is worth pursuing to guarantee a backstop for banks in times of crisis.

I’m no expert, so it’s hard for me to tell how excited I should be about these ideas. While an endorsement by Charles Goodhart is a promising metric in favor of the book, it’s one that might lose meaning if it were to become a target. 😉

But as far as I can tell, the book does an exhaustive job of showing how this framework is supported by nations in various monetary and fiscal situations. The anecdotes above are only a preview – there are plenty more in the book – as well as a solid mathematical reckoning of their underlying dynamics.

I certainly enjoyed the journey, which was my first real in-depth exposure to macroeconomic thinking. It certainly comes with many useful mental models: reliance on indifference conditions, analysis of strategic equilibria in massive flows of capital, or the surprising recurrence of self-fulfilling prophecies. Indeed, whether it be bank runs, the monetary value of emerging markets, or the faith we place in nations’ monetary policies, it’s somewhat alarming the extent to which the world is the way it is simply because we’ve all arbitrarily agreed to have it be the way it is. In any case, I hope Money Capital can help us all agree on what paths to pursue into a brighter economic future. Or at the very least, help brave newcomers who read it better learn, as I hopefully did, more adequate usage of common economics terminology: