More Money Than God: Hedge Funds and the Making of a New Elite, by Sebastian Mallaby

They’re just trying to hedge their bets.

I. Whence All This Money?

Some people are rich for reasons that are very obvious. Taylor Swift made her money from concert tickets and Spotify downloads. Jeff Bezos got rich delivering octopus head scratchers with two-day shipping. Nancy Pelosi made her money by insider trading, and Jeffrey Epstein by blackmailing pedophiles. Some of these things provide more value to society than others.

But what about hedge funds? Why did they get so rich? Unlike Nancy Pelosi, they’re not doing insider trading – and for the most part, they’re not even committing fraud. And yet, they still succeed, making returns higher than index funds, mutual funds, or some investment banks. One might guess their success comes from doing exceptional research on the stocks they buy. Or perhaps they all started with so much capital that they couldn’t help but succeed – after all, in Matthew 25:29, it is written, “For to everyone who has will more be given, and he will have an abundance. But from the one who has not, even what he has will be taken away,” clearly indicating capital has a divine mandate to multiply. But many can do research or pull together $100,000 (very successful hedge funds have been started with just the capital of the founder and a few of his friends), yet billionaires remain relatively few.

In some cases, it is really that simple – hedge funds used specialized research to pick good trades, or traded at more volume than anyone reasonable would think prudent. But in other cases, it feels to me that diagnosing the factors leading to the success or failure of hedge funds is like looking into the biggest cause of sports injuries, expecting it to be “sprained ankles” or something equally mundane, only to discover that a surprising number of athletes are getting their faces ripped off by invisible velociraptors.

In More Money Than God, Sebastian Mallaby investigates the history of hedge funds, and the invisible velociraptors their success depends on outrunning – and also the question of whether hedge funds provide net value to society, or whether we should just let them trip and get eaten. After all, when the economic externalities to society can be so high, it seems worth asking: should hedge funds be allowed to do all this often historically unprecedented trading?

II. The OG Hedge Fund

Only 347 years after the first stock exchange was started by the Dutch East India Company in Amsterdam, the first hedge fund was started by Alfred Winslow Jones. Jones was a Marxist who worked for the US State Department in the 1930s but got kicked out for his association with the German Leninist Organization. In 1949, he needed money and turned to investing, starting what he called a “hedged fund” in reference to his strategy for mitigating investment risk.

Part of why Jones thought he could do better than traditional investors was that he believed there were trends in stock prices based on the behavior of investors, and that he could predict and profit off these trends. In the 1950s, the existence of such trends was in considerable doubt: finance academia had a theory, the so-called “efficient market hypothesis”, which held that all the information about a stock was already in the price, and thus that fluctuations in the stock price were entirely random and impossible to predict. Over the next several decades, billions of dollars of hedge-fund profits proved it definitively wrong – but Jones’s profits were not part of this, since he ultimately had no success in timing the market.

Rather, the effective portion of his investment strategy was the risk mitigation alluded to in the name. The traditional investment strategy was to buy stocks when markets were on the rise, and sell stocks and hold cash when markets were falling. Jones, however, had a strategy that let him make money whether markets were falling or rising, and that did not count on his ability to predict which course they would take. He would buy stocks he thought would rise at faster than market rates, while at the same time shorting stocks he thought would do worse than the market.

(There were some restrictions on shorting stocks in the 1940s, but Jones got around those by being a “private” fund. Shorting stocks is when you borrow a stock from someone who owns it in order to sell it to someone else. Then, you buy it back before you have to return it to the actual owner. If you short a stock, you hope its price will go down, since then you can buy it back more cheaply than you sold it for and the difference is your profit. But if the price of the stock goes up by the time you have to return it to who you borrowed it from, you lose money buying it back.)

With Jones’s strategy, if the market rose, he would lose on the shorted stocks, but would gain more than he had lost on the stocks he held (called “longs”). If the market fell, he would lose on the stocks he held, but would gain more on the stocks he had shorted. This, his theory went, mitigated his risk enough that he could borrow money to invest and still have the same “exposure” to the market as someone who invested less money but only in longs. Both strategies – shorting stocks and borrowing to invest – had been used by investors in the 1920’s, but after the stock market crash in 1929 they had fallen out of favor.

Jones’ strategy of hedging also took into account volatility – that is, some stocks go up a lot when the market goes up, and go down a lot when the market goes down, and some are less volatile and go up and down less. Previously, investors who wanted less risk would buy stocks seen as safe, like AT&T, while investors with an appetite for risk would buy “go-go stocks” like Xerox. But for Jones, volatility could be hedged as well: for example, by buying more of less volatile stock to hedge a smaller proportion of very volatile shorted stock.

Mallaby gives a toy example from one of Jones’s letters, comparing a traditional investor and a Jones-style investor. Both start with $100k, and are targeting $60-$80k exposure to the market. The traditional investor puts $80k into buying stocks and keeps $20k in cash or bonds. The Jones investor borrows $100k additionally, then puts $130k in stocks and $70k in shorts to hedge, which according Jones’s accounting makes for $60k net market exposure.

From here there are two scenarios. Assume first that the market goes up. Jones assumes both investors do a good job picking stocks, so if the market goes up 20%, the longs go up 30% (overperforming the market), while the shorted stocks go up just 10% (underperforming the market). The traditional investor gains 30% on his $80k of stocks and makes $24k profit. The Jones investor makes 30% on his $130k of longs and loses 10% on his $70k of shorts, for a total of $32k net profit.

Now what happens if the market falls? In a scenario where the market falls 20%, the longs go down 10%, and the shorted stocks go down 30% (the more the shorted stocks go down, the better for the investor holding them). The traditional investor loses 10% on his $80k, for an $8k total loss. The Jones investor loses 10% on his $130k of longs but gains 30% on his $70k of shorts, for a final net profit of $8k. Thus, the Jones investor does better no matter whether the market as a whole goes up or down, even while assuming less risk from market exposure: heads I win, tails I still win.

Of course, this is all assuming the investor picks good stocks, which Jones the Marxist was about as good at as he was at timing the market. Instead, he realized that with the right incentive structure, he could get others to do the stock-picking for him. By comparing the performance of individual stocks and shorts to the market as a whole, he could separate out the money he made from a set of stock suggestions into the profit he made just by being in the market when it was going up (“beta”), versus the extra profit from picking good stocks (“alpha”). (Why wouldn’t everyone have been doing this already? Perhaps because it was the 1950s, so all of Jones’s calculations, including the complicated volatility ones, had to be done by hand.) Since this gave him a way to distinguish good stock tips from bad ones, he could pay only those brokers that gave him alpha-generating stock tips, creating an incentive for the brokers to come to him with their best tips first. He also used this method to judge the employees in his fund, creating what Mallaby calls a “competitive multimanager structure” where each manager invested a portion of the portfolio and competed to generate the most alpha. This structure was mimicked by numerous future hedge funds – but though it generated profits in the short-term, it incentivized behavior that was less-than-ideal in the long-term.

Jones’s third innovation was the “performance fee” he charged clients who invested their money with him, taking 20% of the profits. By distinguishing it from other flat fees businesses might charge, he managed to get it taxed at the lower capital gains rate (25%), rather than the income tax rate (91%). Jones did not share this logic with his investors though, instead explaining that: “his profit share was modeled after Phoenician merchants, who kept a fifth of the profits from successful voyages, distributing the rest to their investors.”

These strategies taken together were very successful, and in his first five years Jones made 325% returns, with a cumulative return from 1949 to 1968 of 5,000%. But since his innovations were also fairly simple to imitate, by the 1960s, many of the people who had worked for him went off and created their own funds based on his model. Thus did the hedge fund phenomenon spread from Jones’s original fund, like seeds from a dandelion.

But was this new mode of investing good for the economy? Shorting had been restricted after the market crash in 1929 (in particular, investors were not allowed to short stocks whose price was falling) in an attempt to prevent short-sellers from causing market crashes. But Mallaby argues that this was not an effective rule, and that allowing short-selling is in fact good for markets, since the time short-sellers are doing the short-selling is during bubbles, which helps bring down artificially high prices. And the time the short-sellers are buying back the stocks they short-sold is when the market is at the bottom, which is exactly when everyone else is trying to sell and few are trying to buy. Thus, the short-sellers actually help the market stop crashing. In conclusion, allowing short-selling is a net positive for market equilibrium – at least according to Mallaby.

But hedging is not infallible. There are in general two ways the strategy of hedging – whether that means simultaneously buying and shorting, or other more complex strategies developed by later funds – goes wrong. The first way is hard to avoid, unintuitive, and catches even very smart people. This comes from the fact that many hedging strategies rely on buying positions – stocks, shorts, bonds, futures, whatever – that are independent from one another. This independence allows a fund to cap risk, since even if one or a few of their stocks don’t do what they were expecting, the stocks won’t all act the wrong way at once. Unless, of course, they are not as independent as assumed, which happens when there are what Mallaby calls “unpredictable connections” between them, secret dependencies that are only revealed when some shock to the market knocks everything out of equilibrium. For example, in the 2007 housing bubble, people who sold mortgage insurance assumed that the housing markets in different areas of the country were independent from each other, and thus wouldn’t all crash at the same time – an assumption that proved expensively false.

The second way hedging can go wrong is much simpler. Note that if the markets are going up, it is more profitable in the short-term to just put all your money into buying stocks rather than splitting it between buying and shorting. Thus, it is tempting for hedge funds to, well, just stop hedging. But you can’t reduce risk merely by calling yourself a “hedge fund” – you have to actually do the hedging part too!

What’s going to be cleaned out is your bank account when the market turns.

If you look at Jones’s toy example, you notice that if a third investor borrows the extra $100k and then just buys, and the market goes up, he makes 30% on $200k for a $60k profit, beating the original two investors handily. But if the market goes down, he loses big time – down $20k, more than double the losses of the traditional investor. And in 1969, when the bull market finally shifted, this failure mode is exactly what happened to the not-very-well supervised traders in Jones’s firm, as well as many of the copycat firms. The individual managers had realized that just buying stocks was more profitable, so they had stopped shorting and were no longer “market neutral”. Thus, when the market went down, so did they. The number of hedge funds in the next few years almost halved as all who had forgotten the hedging part took severe losses. The SEC had been considering regulating the growing hedge fund industry, but after the crash wiped out so many of them, they decided the sector was too small to bother. (Regulators finding reasons not to bother with hedge fund regulation is a recurring theme.)

III. Second Generation Hedge Funds

Steinhardt, Fine, Berkowitz & Company

One fund that hedged properly and managed to profit from the bear market in 1969 was Steinhardt, Fine, Berkowitz & Company, started by Michael Steinhardt in 1967. For Steinhardt, the strategy of balancing shorts with longs worked as intended, and his fund lost very little that year. The following years he returned to profiting, correctly predicting when the market would start to rebound.

It was only a few years later when the market crashed again. This time, though, Steinhardt was prepared for the market shift and ready to profit off of it because of the research of one of his employees, Frank Cilluffo. Cilluffo, who joined the fund in 1970, believed in the Kondratiev wave theory of capitalist economies (the finance version of Turchin’s cliodynamics), which predicted – either through piercing insight, or lucky coincidence – an economic crash in precisely the year 1973. Steinhardt shorted heavily in 1972, and when the crash came in 1973, he made out with 41% returns for the year.

Considering how short she is, you’d think she’d be more afraid of a bull.

But Steinhardt did not trust Cilluffo’s market predictions just on the basis of a sketchy Russian theory of market cycles. Cilluffo also was able to call the market crash because of his early recognition of the utility of tracking monetary data – that is, whether banks were lending a lot of money and increasing the money supply, or whether they had stopped lending and the money supply was constant or shrinking. Cilluffo realized that when banks are lending a lot of money and the money supply is increasing, this led to inflation. And when inflation got high, the Federal Reserve was bound to increase interest rates. The high interest rates would in turn prompt investors to take their money out of stocks and put it in banks or bonds instead. And the increase in people selling stocks rather than buying would cause a drop in the stock market. By this chain of reasoning, Cilluffo knew that when banks said they had maxed out their lending capacity, this meant markets were about to go down in a few months. By the 1980s this phenomenon became common knowledge, but at the time Cilluffo’s thinking was ahead of the curve.

However, Steinhardt’s true area of expertise was not timing the market, but block trading. In the 1960s and 1970s, a lot of pension funds and mutual funds were being formed, and these large funds often traded stocks in large blocks. But selling a lot of shares – sometimes hundreds of thousands – all at once, had a very negative affect on the price the seller could get for those shares. Instead of dumping the shares into the open market then, the large institutions would instead sell to brokers who specialized in dealing with trading large blocks of stock. The funds would still sell them at a discount, but would get a better price than otherwise, since the brokers had connections and knowledge that would allow them to resell the shares closer to market price. Steinhardt developed a reputation for dealing in block sales, which caused the pensions and mutual funds to come to him preferentially. He was then able to resell the shares for more than he had paid, using his connections with the two main banks that had gotten into the business of block sales, Oppenheimer and Goldman Sachs. In addition, he had practice and connections dealing in the “third market”, where through a regulatory loophole large blocks of stock could be traded without those trades being recorded (so no one knew how much they were selling for). There was a dark side to this: some of his unusual profits were due to brokers giving him “tips” about the clients they were selling on behalf of, otherwise known as illegal collusion – though he was never convicted of this.

The combination of these strategies made Steinhardt’s fund very successful, and from 1967 to 1978 they made 1200% returns, even while US markets as a whole were up only 170% over the same 11 years – a performance all the more impressive considering that they were trading during a period of multiple market downturns. Jones, in comparison, had profited off a long stretch of practically uninterrupted bull market.

While Mallaby believes Steinhardt’s unusual profits were entirely explained by his success in market timing and expertise in block trading, he notes that the managers of hedge funds often give other explanations for their success. Steinhardt himself thought that his high returns were due to his company’s culture of “intensity” – Steinhardt apparently had an intercom system that he would use to broadcast himself to the whole office whenever he screamed at associates who made mistakes. Mallaby is ambivalent about whether this actually helped their success, or whether their success might have come in spite of these practices.

Of course, the money Steinhardt was making had to come from somewhere, and in the case of block-trading it was from the pension and mutual funds who sold him their shares at a discount. But Mallaby thinks that overall, Steinhard’s trading benefitted the funds he bought from, since without people willing to buy and sell large blocks of stocks, the pension funds and mutual funds would have had to sell their shares on the open market – as they always could have done anyways – but where they would have gotten even worse prices for such large blocks of shares. Mallaby goes so far as to claim the fund’s trading was “unambiguously good for the stability of the financial system. The partnership’s contrarianism made a small contribution toward dampening the disruptive swings in stock prices. [They] sold during the bubble of 1972; [they] went long at the end of 1974, when the post-crash market was desperately in need of buyers. Likewise, by pioneering the application of monetary analysis to stock markets…Tony Cilluffo’s analytical techniques made such bubbles less likely in the future.” Though if the rest of Mallaby’s book is describing a future where bubbles are less likely, I’d hate to see the counterfactual.

Commodities Corporation

Commodities Corporation was started by F. Helmut Weymar and other backing investors in 1970, and his main strategy was trading in – suspense! – commodities. Weymar’s main innovation was to use computer models to make these predictions.

Now, there are two ways to get ahead of the market. The first is to predict future price movements based on knowledge of the real world – for example, the yield of next year’s corn harvest. The second is to predict future prices based on trends in past prices – that is, to ignore fundamentals and instead use the market to predict itself.

Weymar’s early computer models used the first method: they predicted the prices of commodities based on underlying factors like weather, historical data, and economic conditions. (His fund’s commodities of interest included cocoa (Weymar’s own area of expertise), wheat, pork belly, soybeans, and feed grains.) Yet this strategy had limitations, since the real world is inherently unpredictable. At one point, they used their model’s predictions to buy corn futures, only to then start hearing rumors about a corn blight. After they saw reporting hyping up the severity of the blight on TV, they panicked and sold all their futures when prices were at the market bottom, even though the blight turned out to be a false alarm. Since they had borrowed significant money to bet on corn futures, this resulted in considerable losses for the firm.

Thus burned, they turned to the second method: modeling market trends. Another Commodities Corporation associate, Frank Vannerson, created their trend-following model, called “Technical Computer System”. The basic idea was that stocks had trends, so investors could profit if they “buy things that have just gone up on the theory that they will continue to go up; short things that have just gone down on the theory that they will continue to go down.” Another benefit of using a computer model of this sort was that it could take into account risk and limit the leverage (how much money they borrowed to invest) on riskier trades. This model led to greater profits for the fund.

Another area where Commodities Corporation profited was currency speculation. Though trading currencies was not yet popular among hedge funds, the Commodities Corporation associate Michael Marcus was ahead of the times and made a lot of money on a trade involving the riyal, Saudi Arabia’s currency. In early 1975, Saudia Arabia had their currency pegged to the US dollar, but as their exports increased, this put upward pressure on their currency and risked causing inflation in Saudi Arabia if they didn’t revalue. Marcus saw that he could buy the riyal without risk, since if Saudi Arabia revalued, the riyal would go up and he would make a lot of money. But even if Saudi Arabia managed to keep the peg, the riyal certainly wouldn’t be devalued, so he couldn’t lose much money either. In March 1973, Saudi Arabia did revalue, and Marcus made a killing. This asymmetry in trades with little risk and high potential profit is part of what made currency speculation so popular among hedge funds in the coming decades.

While trend-following models were somewhat more complicated to copy than the basics of Jones’s strategy, they were still well within the realm of imitation, and many traders at Commodities Corporation started to break off and start their own funds. The dandelion infestation of hedge funds continued to spread.

Tiger Management

Around the 1980s, the hedge fund industry was dominated by three big funds. One was Steinhardt, Fine, and Berkowitz. Another was the Quantum fund under Soros Fund Management, founded by George Soros.

The third was Tiger Management, started by Julian Robertson in the 1980s. In one way, the success of Tiger is the easiest to explain, since they simply invested based on the Jones model of buying good stocks while shorting bad ones as a hedge. They would judge stocks based on their fundamentals, looking at their balance sheets, employees, etc. and then invest in stocks that they believed to be undervalued, and short those that were overvalued. After a few years, once all the other investors saw the results of Robinson’s chosen companies and realized what Robertson and the managers under him had discovered years earlier, the stock prices would revert to reflect the actual value of the companies, and Robertson would profit.

In another way, the success of Tiger was mysterious, since they don’t seem to have been doing anything special. Mallaby himself seems a bit confused as to what their secret sauce might have been, deferring to Robertson’s own explanation – that his employees were very motivated because of the fund’s “culture”. Whatever the real reason, Robertson’s fund was very profitable: from 1980 to 1998, his returns were 31.7% per year on average. Many of his managers went off and founded their own funds as well.

Ultimately, though, the pure stock-picking strategy had its limitations. Robertson failed to predict the next crash in 1987 and suffered losses, finding himself in the same boat as Soros and Steinhardt.

Tudor Investment Corporation

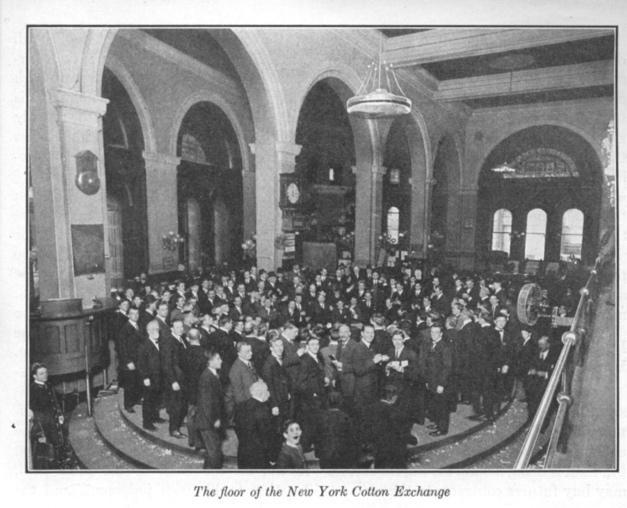

But even if the big three hedge funds failed to predict the next crash, not everyone found themselves underwater. One fund that profited was Tudor Investment Corporation, started by Paul Tudor Jones II in 1983. (Note that this is a different Jones than the Alfred Winslow Jones who started the first hedge fund, which is possibly the reason Mallaby keeps referring to hedge fund managers by including their middle names the same way the media does for serial killers.) P.T. Jones had started in finance working as a floor trader on the New York Cotton Exchange, which had given him a feel for the way markets went up and down. His trading strategy reflected this, and was based on guessing what the markets were going to do and “riding market waves”. This was different than Commodities Corporation’s strategy in that he didn’t use computer models, just research and intuition.

The New York Cotton Exchange before computers, back when prices were determined the way God intended: by people yelling at each other.

His hedging strategy was also different than the original A.W. Jones style traders, who hedged longs with shorts. P.T. Jones’s strategy was based instead on market asymmetry. Specifically, he recognized that shorting the market when a crash was expected was a low-risk, high-reward strategy. If the market did crash, then he was in a position to rake in massive profits. But even if the market didn’t crash, it certainly wouldn’t go up, which meant he wouldn’t lose very much when he went to buy back his shorted stocks either. (Part of the reason this worked so well for Tudor Investment but not later funds was that his fund was small in the scheme of things – when hedge funds started borrowing against their assets to hold billion-dollar or bigger positions, it became impossible for them to get out of the market without influencing the market against themselves.)

Since P.T. Jones’s strategy relied on anticipating market crashes, his vigilance led him to predict the 1987 Black Monday crash, unlike many others – that, and his belief in the ever-popular Kondratiev wave theory. Besides shorting stocks, he profited additionally off of the crash by guessing what the Fed would do, in the same way Steinhard and Cilluffo had in 1973. During the crash, he predicted correctly that the Fed would prop up banks, which increased the value of bonds; trading on that information made him between $80 and $100 million.

And his crash-predicting capabilities were not confined to the United States. In 1990, he predicted a market crash in Japan by reasoning through the logic of Japanese investors and the impacts of their actions on the market. He knew that most Japanese investment funds had the same 8% target rate for yearly returns. If the market had dipped at the end of the year, these funds might not bother to sell stocks, since the market was up enough over the course of the year they would still make their returns threshold. But when the market dipped in January, he saw that they would decide they weren’t going to risk market exposure when it might cause them to miss their target rates, and would instead switch to investing in bonds that would provide relatively safe returns for the rest of the year. This behavior at a large scale took a small downward market blip and turned it into a full-blown crash. P.T. Jones’s prediction was so accurate that Tudor Investment made over 80% returns that year.

Sometimes just predicting trends was not enough for him – when the conditions were right, he would also start them himself:

“In the spring of 1987, Jones decided it was silver’s moment. Gold had already staged a rally, and silver usually followed; besides, there were rumors that output at key mines might be disrupted. Early on a March morning, Jones executed a pincer movement worthy of his hero, General George S. Patton: He bought a gutsy position in silver futures, buying up contracts from floor traders and leaving them all short; then he bought physical silver from four dealers. Soon the dealers were doing precisely what Jones expected them to do. Because they understood that gold had already rallied and silver was positioned to follow, the dealers didn’t want to be caught with depleted inventories; they immediately phoned the silver exchange with purchase orders to replace what they had sold to Jones some minutes earlier. When their phone calls reached the exchange, the dealers were in for a surprise: The traders who would usually have had silver futures to offload had already sold out to Tudor. The traders, for their part, followed Jones’s script too. When the dealers called them with urgent buy orders, they assumed that the rumors of a supply disruption must have come true, and they rushed to buy back some of the contracts that they had sold to Jones earlier. Before very long, pandemonium broke out; the speculators and dealers whom Jones had left short were scrambling to protect themselves from spiking prices, driving those prices up further as they did so. By sensing when the market was poised for a rally and having the guts to give it a kick start, Jones made off with a handsome profit.”

But is it good for markets to have someone out there starting market trends just for his own profit? Mallaby says this was not a problem: after all, the strategy had its limits, and Jones himself admitted he couldn’t shock the market into trends that weren’t already primed to start. And Jones’s other strategy of trading against people who needed to meet certain institutional requirements, like the Japanese investors, was also net positive in Mallaby’s view: he was “[providing] liquidity when it was needed”.

IV. Why Currencies Fear George Soros

Born in Hungary, George Soros survived World War II on the continent, before moving to London and then New York, where he founded his own hedge fund, Soros Investment Management, in the 1970’s. Soros traded based on his theory of “reflexivity”, which held that market trends were mainly determined by investors’ beliefs and actions, rather than fundamentals.

In 1985, this theory led him to make a very large and successful bet against the US dollar. Soros saw that despite the US running a large trade deficit, the dollar was still strong. Based on reflexivity, he guessed that the cause for this paradox was nothing fundamental about the dollar, but rather a trend among investors that was keeping the dollar popular. Since there was no underlying fundamental force driving the trend, it was due to reverse at any time. By 1985, when Soros believed the trend was on the verge of reversing, he owned $720 million worth of foreign currency of all types – $73 million more than the equity in his fund at the time. (The way this trade works is that if you think a currency, say the dollar, is about to lose a lot of value compared to other currencies, say the yen, you use dollars to buy yen while the dollars are still valuable. Then after the dollar loses its value, you use your yen to buy a bunch of dollars back on the cheap, thus ending up with more dollars than you started with.) When Soros’s prediction came true and the dollar dropped, he profited to the tune of $230 million. Yet, making a bet this big was a risky strategy. Mallaby quotes Soros’s stance on the risk he took: “As a general rule, I try not to exceed 100 percent of the Fund’s equity capital in any one market, but I tend to adjust my definition of what constitutes a market to suit my current thinking.” Unfortunately for him, this flexibility of thinking did not help him in the 1987 crash. He had not been expecting it, and when he tried to get out of his positions, he found that his fund was too large a portion of the market for him to sell out without shifting the market even more strongly against himself.

Europe and the British Pound

In 1988, partly due to their poor results in 1987, Soros turned management of his Quantum fund over to Stan Druckenmiller, who continued to trade in currencies.

In 1990, the fall of the Berlin Wall created an opportunity for Druckenmiller to profit. Most investors were expecting Germany’s currency, the deutsch mark, to not do well, because the West German government that was issuing the marks was also expected to run a budget deficit, and common sense held that budget deficits led to inflation. However, Druckenmiller realized that the German Central Bank was very conservative and would certainly raise interest rates, which would cause the deutsch mark to go up instead. Druckenmiller bought marks and did very well – Quantum made a 29.8% return in 1990.

During the 1992 European Exchange Rate crisis, Europe’s misfortunes became yet another opportunity for Quantum to profit. The crisis originated from the fact that interest rates in Germany were very high, but other countries did not want to raise their interest rates as much. The Europeans had an agreement, the European Monetary System, where they had semi-pegged their currencies to each other, so that they traded against each other but only within a certain band. But because of Germany’s high interest rates, the deutsch mark was trading a lot higher than many other currencies, and the others were falling to the bottom of the band.

There were several strategies a country could use to keep the value of its currency within the band. It could attempt to attract foreign investment. It could raise its exports. It could raise interest rates. It could dip into its foreign reserves to buy its own currency at a price at or above the bottom of the band (this effectively increased demand for the currency while decreasing supply, thus driving the price up – it feels strange to think of currencies as having a “price”, but that’s how exchange rates work). And as a last resort, if all else failed, the country would be forced to devalue, and let the currency drop to an exchange rate below that specified by the European Monetary System.

The first currency to devalue was the Italian lira. Germany, in accordance with the European agreement, spent $15.4 billion buying lira to prop it up, but ultimately was overcome by the massive amounts of hedge funds, investors, and speculators of all sorts who were expecting the lira to devalue and shorted it relentlessly. Luckily for Italy, the lira came to the edge of failing on a Friday, giving the Italians all weekend while the markets were closed to negotiate a deal where they could let the lira devalue but still stay within the European Monetary System.

The British were not so lucky. They were falsely confident that they could get away with just buying more pounds in order to keep their currency within the exchange band, and they borrowed $14 billion to do this. But unbeknownst to them, investors were waiting to short-sell pounds in staggering amounts. Just Quantum alone was planning to short-sell $15 billion worth. When the pound started to fall, the British central bank was bound by the European agreement to buy its currency at the exchange rate at the bottom of the band – even though at this point it was much higher than the pounds were worth. Quantum and other funds sold pounds to the British central bank at this artificially high value in massive amounts, as much as they could convince anyone to lend to them.

When the British finance minister, Norman Lamont, figured out that this was unsustainable, he went to the prime minister. But the British prime minister, John Major, was more interested in sharing the blame around than actually fixing the problem and dragged his feet, resulting in the British central bank buying pounds for more than they were worth for several days longer. When Major finally agreed that they would raise interest rates, first 2%, then another 3%, it was too little, too late. At last Major agreed they could no longer afford to drain their foreign currency reserves buying pounds, but by that point it was a Wednesday – thus, there was no time to negotiate a devaluation, and Britain had to exit the European exchange-rate agreement altogether.

Ultimately, the Bank of England spent $27 billion buying pounds, which fell 14% against the deutsch mark when the currency was allowed to float, coming out to a $3.8 billion loss. Mallaby lays the blame for this “vast financial transfer from its long-suffering taxpayers to a global army of traders” solely at the feet of John Major, who he thinks should have devalued the currency immediately and thus prevented the losses. And yet, a large part of why the pound fell so quickly is that Druckenmiller and Soros, as well as other funds, went all-out with shorting the pound. At one point, Soros told Druckenmiller to “go for the jugular”. Overall, Quantum managed to short-sell about $10 billion worth in pounds, and made over $1 billion in profits. They also profited from buying British bonds and equities, since they realized correctly these were going to go up after the currency was allowed to float.

Quantum made another $1 billion when the Swedish krona was devalued. Sweden managed to stave off the problem for a bit by raising their interest rates first to 75%, and eventually to 500%, but ultimately went the way of the rest.

France did not have to devalue, which Soros also correctly predicted, and thus he did not bother to short the franc. Though, as Mallaby describes, Soros told the story a bit differently: “Shortly after the pound’s devaluation Soros saw Jean-Claude Trichet, the governor of the French central bank, and told him that, out of concern for the destabilizing effects of his own trading, he would not attack the franc. This claim to selflessness was a bit much, since Quantum had correctly calculated that the franc would hold and was about to make a killing on this prophecy.”

Mallaby is adamant that the blame for Europe’s currency devaluations should not be laid at the feet of the hedge funds and speculators that shorted them. In his view, the currencies were misvalued, and hence deserved to be devalued, and the speculators only hastened the inevitable. And yet, I have to ask – is pegging currencies such a sin? Despite the risks and costs, countries continue to do it because it brings them benefits, such as creating stability, promoting trade, and controlling inflation. Is having efficient and correctly priced markets more important than these things, such that those countries that try it deserve to have hedge funds and speculators run off with their lunch money? Also, Mallaby’s implication that attempting to maintain a currency peg is futile is not borne out by history. His own book even provides a counterexample: France, which never had to devalue. Another example is Hong Kong, which pegged their dollar to the US dollar in 1983. They held this peg through the 1997 Asian financial crisis, despite strong pressure to devalue, by raising interest rates and spending $1 billion in foreign currency reserves – and ultimately succeeded in maintaining the peg. In a hypothetical world where hedge funds and speculators had not piled in to trade against them, would all of these European nations still have been forced to devalue? France managed to get through the crisis without devaluing, but did investors not bet against the franc because it was strong enough, or did the franc make it through because investors didn’t bet against it – a self-fulfilling prophecy?

Either way, Mallaby considers the currency problem solved for Europe; the first solution tried, currency controls, he was not impressed by, but he considers the European nations unifying their currencies into the Euro to have been the perfect fix.

Asia and the Thai Baht

Hedge funds got involved in Asia and Russia during the 1990s when these places started to open up to more foreign investments. However, this was a risky business. It was tempting to invest in these expanding markets, especially for funds like Quantum that had grown to such a size they could no longer make maximal returns in western markets (it’s hard to leverage yourself up and invest multiples of your fund’s assets in a trade when your fund’s assets run in the billions of dollars – or if you did, your money would make up a majority of the market, an extremely dangerous position to be in). But investing in Russia and Asia was also treacherous, since government controls and a dearth of buyers there could make it difficult to get out of the market if things went poorly.

Yet despite the danger, hedge funds invested anyways, sensing opportunity. As it turned out, maintaining currency exchange rates was not only a first-world problem. And for developing nations, as for European nations, the ever-dependable Soros was there to make it worse.

In 1997, Thailand’s currency, the baht, was pegged to the US dollar. But Thailand’s exports were decreasing, causing a trade deficit, and meanwhile the dollar was strong. At first, Thailand got loans to cover the difference from their trade deficit, but the loans had interest, and foreign investment dropped as Thailand’s economic outlook worsened. Normally the solution to this problem would be to raise interest rates, but the Thai needed to keep their interest rates low out of fear for their shaky banking sector. These factors combined to put downward pressure on the value of the baht, making the peg difficult to maintain.

Around this time, Arminio Fraga, working for Quantum, went to Thailand to talk to central bank officials. One bank official rather unwisely admitted to him that they were indeed having issues, but they would rather devalue the baht than raise interest rates. This admission made it clear that a devaluation was all but inevitable, and made it safe for Quantum to short the baht – which they did to the tune of about $2 billion.

Mallaby notes that if they had shorted more, or if they had borrowed to short a multiple of the fund’s assets (as they did when they shorted the pound), then they could have forced Thailand to devalue immediately. But Soros did not want to do that. Mallaby, who read Soros’s published diaries, takes Soros at his word that he had moral reasons for not “going for the jugular” again. When he shorted the baht this time, he was just trying to help. Mallaby explains the logic thusly: “…speculation could benefit poor societies if it served as a signal, not a sledgehammer. The function of the virtuous speculator was to alert governments to the need for change – in Thailand’s case, that the baht had to devalue. This signaling could avoid hardship for ordinary people, since the more a government procrastinated about devaluation, the more brutal the eventual currency collapse would be.” The idea was to make the government give up and devalue their currency before they wasted all their foreign reserves trying to defend it. But this logic only works if the government in question actually agrees to devalue before they’ve drained their foreign reserves.

Apparently this reasoning did not appeal to the Thai government, who instead doubled down on defending the baht. In an effort to stop the speculators, they forbid their banks to lend baht outside Thailand. Unfortunately for the Thai, this did not manage to stop speculators; instead, it just raised the interest rates the speculators had to pay to borrow baht to short. (At one point the interest rates were so high Tiger Management was paying $10 million dollars a day to hold their multi-billion dollar short position.) In the end, despite Soros’s magnanimous forbearance, Thailand drained their foreign currency reserves to defend the baht, only giving up when they ran out of money after Tiger went on a final shorting spree. After devaluation, the baht fell 32% against the dollar. Soros made $750 million from the trade, while Tiger made around $300 million. Joining the George-Soros-Crashed-My-Currency Country Club did not do wonders for Thailand’s economy, though Mallaby argues that “speculators had merely forced an adjustment that was ultimately inevitable.”

Thai baht notes. The guy on them is King Bhumibol Adulyadej (Rama IX). If I were a king, I also wouldn’t want to let a currency with my face on it devalue.

This sort of currency shorting, especially in developing economies, was very unpopular among the western political class (not to mention the political class in developing countries) and made hedge funds reviled. Soros, meanwhile, wanted to be seen as a statesman and a philanthropist, and eventually this desire won out over the desire to actually make money from trades. As the Asian financial crisis continued, Soros stopped trying to short currencies. In Indonesia, he bought rupiah instead of shorting, and lost $800 million while holding rupiah even as it collapsed – though after a certain point it was impossible for him to get out of the position anyways, since no one was buying.

This collapse in Indonesia had knock-on effects in South Korea, since they had lent a lot of money to firms in Indonesia. Their central bank was also using some creative accounting to total up their foreign reserves, counting reserves that had already been promised elsewhere, and thus making their position even worse than it at first appeared. Soros’s firm knew about this from their investigations, but Soros still did not try to short their currency – not even a little bit of shorting, not even just a measly $2 billion worth of shorting – zip, nada, nothing. In his journals, Soros attributes his decisions here to his “messiah complex”. Ah yes, just like how in the bible Jesus gave up his opportunity to make thirty pieces of silver to…wait…

1992 printing of the Indonesian rupiah. There should be a rule that pretty currencies can’t be devalued.

Really though, Soros was taking big losses in some of these countries as well. For example, in Russia, Soros bought a billion-dollar share of Svyazinvest, a partially-privatized Russian telephone company. This trade was a poor one for a hedge fund, since it wasn’t something he would be able to get out of quickly, but his bidding on the company helped Russia raise much-needed capital. He also secretly lent hundreds of millions of dollars to Yeltsin as a bridge loan. When this first loan was not enough, Yeltsin went to Soros again in 1997, trying to get another bridge loan of $7 billion. That was a bit much even for Soros, who tried instead to help Yeltsin raise it from US and European banks and officials, though his efforts met with no success. Ultimately, he wrote an open letter attempting to help Yeltsin get the loan, but investors interpreted the letter to mean instead that Soros had shorted the ruble. This caused others to copy Soros’s non-existent trade, and forced the ruble to devalue; though in fact, Soros had not shorted the ruble and lost another few billion dollars in his Russia portfolio from the devaluation.

V. Recessions, Recessions

The 1994 Bond Bubble and Askin Capital Management

Alan Greenspan, chairman of the Federal Reserve, did not set out to start a recession when he raised interest rates from 3% to 3.25% in 1994. But he didn’t realize the effect the policy would have, because the logic of how markets responded had been fundamentally changed by the trading strategies of the investors of the day, investors which included many hedge funds. One of the problems with hedge funds that even Mallaby recognizes is that they make “unpredictable connections” between markets that can make the effects of government policy on markets equally unpredictable.

So, what were these trading strategies that so fundamentally overturned the traditional market logic that Greenspan was counting on?

The purpose of banks is to borrow short (from individuals or other banks), and lend long (to people needing mortgages, small businesses needing loans, and so forth). This is most profitable when interest rates are low, so in the 1990s, when the economy was doing poorly, the Fed kept the interest rates low in order to encourage banks to do more of what they are best at and thereby help the economy.

However, what is profitable for banks is often profitable for other investors as well. Hedge funds decided they were going to do the same thing, acting as “shadow banks”. But hedge funds don’t go out and get customers the same way banks do. Instead, their short-term borrowing came from brokers, and their version of long-term lending was buying long-term bonds. This sort of business was not quite as helpful to the economy as what the banks were doing; it was, however, very profitable for the hedge funds.

There was another difference between hedge funds and banks as well: banks had stricter rules about their asset ratio, that is, what proportion of the capital they borrowed they had to have set aside to make sure they could pay back their loans. For banks, this was about 10%. For hedge funds, their only limit was what brokers were willing to lend them, and many of them could convince brokers to let them set aside as little as 1%. Since so many hedge funds were borrowing so much money in this way to buy long-term bonds, it began to affect the bond market. Effectively, this caused short-term interest rates to feed through into long-term bonds, creating a bond bubble. In hindsight, there might have been some signs that hedge funds were buying too many bonds – such as not letting themselves be capped by natural limits like, say, the number of bonds actually issued:

“In the April 1991 Treasury bond auction, Steinhardt and Bruce Kovner between them bid for $6.5 billion of the $12 billion worth of paper that was due to be issued; then they lent these bonds to short sellers and bought them back again, ending up with $16 billion of bonds – considerably more, in other words, than 100 percent of the market. As the bonds shot up in value, the short sellers tried to get out; but they couldn’t buy back the paper because Steinhardt and Kovner had cornered the market, and they were not selling.”

Bonds are “fixed income securities”. Someone who wants to raise money in the present sells a bond to someone who wants to invest. To get people to buy the bond, the bond pays a fixed amount of interest at set periods, and the entirety of the principle is paid back at the end of the whole period. Traditionally, the amount bonds are worth on the market goes down when inflation is high, since investors think they can make more money investing in something that is tied to inflation – that is, the bond is worth less compared to, say, stocks, whose price will inflate along with the rest of the economy, whereas with bonds the payout is fixed no matter what inflation does. But when inflation is low, the fixed payout of bonds is closer to what investors would get from stocks anyways, but with the added benefit of being “safe” (since bonds are guaranteed to pay out as long as the issuer doesn’t go bankrupt, and even then, bondholders are secured creditors and paid before stockholders or vendors in bankruptcy proceedings); thus, more people want to invest in them, so their price goes up. But bonds are also subject to basic laws of supply and demand like everything else, so if some other factor causes people to want to sell bonds – such as a liquidity squeeze among investors who own a lot of bonds, like, for example, hedge funds – then their price will go down since more people are selling than buying.

When Greenspan raised interest rates expecting that he could do so without overly affecting the markets, his assumption was not without historical precedent. He thought raising interest rates would signal lower inflation in the future, which traditionally causes bonds to rise. But the hedge funds were not the usual historical investors. To them, rising interest rates signaled market uncertainty and risk – and in an uncertain market, they all suddenly realized that they were over-leveraged. This was exacerbated when the yen, which many hedge funds had been shorting, suddenly rose. And when the hedge funds started losing money, the brokers who had lent them the money became worried and demanded higher asset ratios – that is, the funds started getting margin called. The hedge funds needed to get their capital out of the market fast, and to do this they sold bonds – a lot of bonds. As Mallaby explains: “If you are leveraged one hundred to one, and if your broker demands an extra $4 million in margin, you have to sell $400 million worth of bonds – quickly.”

Unfortunately for the hedge funds, when they went to sell their bonds, they found that everyone else already had the same idea. The trade had become “crowded” – that is, the individual hedge funds had all converged on the same investment strategy without realizing they were doing so. And when everyone is selling and no one is buying, price drops fast; thus completing the tale of how poor Alan Greenspan inadvertently caused a crash in the bond market by raising interest rates.

“Well, well, well, if it isn’t the consequences of my own monetary policy.”

But the “unpredictable connections” did not stop there – European bonds dropped as well, even though European interest rates were unaffected by the US Fed’s decision-making, merely because the hedge funds that had bought US bonds had also bought European bonds and were now rapidly selling both.

The biggest hedge fund that got liquidated in this crisis was Askin Capital Management, started by David Askin, which specialized in dealing with mortgages. Its business was slicing mortgages into interest only (IO) strips and principle only (PO) strips, on the theory they traded differently based on who would pay off a mortgage early. It also traded in combinations of these IOs and POs, making “inverse IO”s and “inverse PO”s, including one called a “forward inverse IO” that Mallaby does not explain, perhaps because it is not relevant, perhaps because it is an abomination against gods and men that would make Aristotle turn in his grave. (Aristotle likely would not have been impressed with hedge funds in general, given that he wrote that “retail trade…is justly censured; for it is unnatural, and a mode by which men gain from one another. The most hated sort, and with the greatest reason, is usury, which makes a gain out of money itself, and not from the natural object of it. For money was intended to be used in exchange, but not to increase at interest.”)

Askin told his investors that he had created a model to calculate his risk, which guaranteed his mortgage jerky strips would profit no matter whether markets went up or down. This was a complete lie – he had made no such model (not that it would necessarily have helped him if he had, as Long-Term Capital Management was soon to discover). During the popping of the bond bubble, many hedge funds were having hedging-failure problems of the first sort mentioned earlier, where connections exist where they weren’t expected, causing independent trades to become all too dependent in times of crisis and ruining best-laid hedging strategies. Askin, on the other hand, had made a failure of the second sort: he had not bothered to hedge at all in the first place, and when a crisis hit, he paid the price. At one point, Mallaby suggests that hedge funds could be called “edge funds” in the sense that they have an investment edge over everyone else. But some of them seem more like “edge funds” in that they’re standing at the edge of a cliff, and all it takes is a little push for them to have a big fall. And Askin’s was the edgiest edge fund of them all (at least in the early 1990’s). When the Fed raised the interest rates, the mortgage market dropped, and Askin’s fund fell sharply. All his brokers and creditors called him up, and when he couldn’t come up with the money to meet the margin calls, his fund was liquidated and the lien-holders scrambled to get their money out before everything was gone.

Of course, Mallaby places the blame for this entirely-leveraged-hedge-fund-caused catastrophe squarely on the Fed, making the astonishing suggestion that the Fed should have deviated from its historical mandate to use interest rates to keep both inflation and unemployment low, and instead should have used interest rates to deflate the bubble in the bond market. In my opinion, some rules stopping hedge funds from leveraging themselves by factor of a hundred might have worked as well, but what do I know.

Actually, Mallaby is not just ignoring common sense here, but also the advice of the possibly evil but undeniably financially knowledgeable George Soros, who was called in to testify in hearings before the House Financial Services Committee about the bond market disaster. Soros’s conclusion was that hedge funds weren’t the only problem, since they weren’t the only ones leveraging, and that if Congress were going to do something about it they ought to restrict leverage for everyone. But making rules for everyone was hard: Mallaby chalked Congress’s inaction up to a mindset where “in the absence of an action plan [they found it convenient to] assert that no action is needed.” Somehow every time the opportunity to regulate hedge funds arises, the would-be regulators always find a reason to not do so.

The 1997 Asian Financial Crisis and Long-Term Capital Management

Though Soros’s fund took losses in the 1997 Asian financial crisis by investing in currencies and countries where the currency was ultimately devalued, Soros was no fool, and his fund had more than enough capital to survive these losses. This was not the case for everyone.

Long-Term Capital Management was founded by John Meriwether in 1991, after Meriwether was forced to resign from Salomon Brothers when one of the people he was overseeing got caught by the SEC for cheating in Treasury auctions. The primary strategy of his fund was bond arbitrage. He would find bonds that are similar in terms of the issuer, interest, and principle, that in theory should pay out the same and thus be worth the same, but because some of them were easier to buy and sell (that is, more liquid) than others, a gap emerged where the less liquid bonds were cheaper than the more liquid bonds. For example, newer Treasuries had a bigger market of buyers and sellers and so were more liquid, and thus cheaper, than older treasuries. A liquidity gap also existed between “different bonds of the same maturity, between a bond and the futures contract that was based on it, between Treasury and mortgage-backed bonds or between bonds in different currencies”. Meriwether would then buy the cheap ones and short the expensive ones, since according to his “Slinky theory” even if the values diverged because of shocks, they would ultimately “spring back” and LTCM would make money.

But buying or shorting bonds with low liquidity is definitionally risky, since you cannot sell or rebuy them quickly if you need to get out of a position. And yet, LTCM operated with very high leverage. Meriwether dared to do this because he thought he had his risk all calculated out. He had recruited PhDs and Nobel prize-winning economists and made a model of “value at risk” based on the potential losses he thought the fund might have based on historical data and their guesses about what potential shocks might happen.

Unfortunately, calculating risk is very hard, and his economists did not quite manage to discern all the “unpredictable connections” that plague markets where hedge funds are at play. They failed to realize that, when all the firms were doing the same set of trades, that made the trades correlated within the markets even if they had nothing to do with each other in their fundamentals. This meant that if a bunch of funds needed liquidity simultaneously, they would dump all their positions at the same time – across all markets they had invested in. This wouldn’t be a problem for a fund that was doing trades no one else knew about. But LTCM’s trades had become crowded, as other funds, unbeknownst to LTCM, had copied them.

When the market was peaceful, LTCM’s models worked as intended, and their trades profited. But when the baht devalued and Russia defaulted on its debts, this caused market panic. The “liquidity premium” LTCM was trading on was highest when markets were panicking and people needed to buy and sell right away. This drove the arbitrages LTCM was betting would converge to instead spread a lot wider and not spring back. This in turn meant they lost more money than their models had predicted was possible, and since they were so leveraged, they had a big problem. They tried to raise money, but calling around to ask for capital signaled to the other funds and investors that they were having problems, prompting other speculators to trade against them instead, and making their problems worse rather than better. They even asked Goldman to buy them, but Goldman asked to see their portfolio first, and then instead of buying them just traded against all their trades (which was illegal, and Goldman claimed it hadn’t done that, but Mallaby doesn’t believe them, and neither do I).

LTCM had such a large portfolio, $120 billion, that it owned very large fractions of some of the markets it was trading in. Thus, if LTCM went bankrupt and the brokers and lien-holders that had lent to it sold all the bonds it had been holding at once, it would completely crash these markets, and no one wanted this to happen. So when LTCM realized they were cooked, they went to the New York Fed, and the second in command there (since the head guy was out of town), Peter Fisher, brokered a deal between LTCM’s counterparties to buy it and prevent it from going under and causing a market crash. This negotiation was not without some difficulties, as none of the banks wanted to cough up the cash, preferring to free-ride if possible. However, they all realized a market crash would be even worse, and ultimately a compromise was reached.

Afterwards, there were congressional hearings about the bond crash and whether LTCM’s near-disaster and the crash itself could have been prevented by better regulations on hedge-funds. Once again, no action was taken. The conclusion reached was that “private creditors would check hedge fund excesses”. Again, the argument was that this was not merely a hedge-fund problem, and it was better to regulate either everyone or no one. (The investment bank Lehman Brothers had been suffering from much the same problems as LTCM, which was part of the reason they were so unwilling to contribute to buying LTCM and caused problems for Fisher in the negotiations.)

Once more, the obvious solution is that the regulators should have capped leverage. But Mallaby argues it isn’t so simple: the amount of leverage that is safe varies depending on firms’ investment strategies, how much they are hedging, what derivatives they are buying, and is just not an easy thing to calculate in general (as LTCM found out very painfully). The Europeans made a set of standards trying to do this, Basel II, which proved incapable of protecting their firms in the 2007 financial crisis. Mallaby thinks any attempt to regulate leverage in the US would have worked just as poorly.

Mallaby says that unless the US wants to go back to the old days when banks had to hold 40% worth of their assets in capital, capping leverage will not work. And for Mallaby, that is no solution at all, because such a policy would decrease lending and investment and slow economic growth. (This itself implies Mallaby thinks regular market crashes are a fair price to pay for somewhat higher long-term economic growth. This sounds like the opinion of someone who profited in the last market crash, but I haven’t seen his portfolio so I can’t say.)

The 1999 Dot-Com Bubble

Steinhardt ended up closing his fund after taking big losses in the 1994 bond bubble. But Soros’s and Robertson’s funds were still investing when the dot-com tech stock bubble rose in 1999. They all realized it was a bubble, of course, but it was not worth it for them to short tech stocks since they didn’t know when the bubble would pop.

Investing in tech stocks made no sense for Roberson’s value-investment strategy, since value investing was based on looking at balance sheets, and overvalued tech stocks had no profits or assets. He stayed out of the tech market, but as the tech market took over more and more of the general market, his fund started to do poorly. Tiger Management had grown too large, causing Robinson difficulties in finding investments large enough to generate significant returns on his capital. This led to him holding onto some stocks for too long, and when he began to take heavy losses on trades where he was a significant fraction of the market and could not get out, he chose to return his investors’ money and close his fund rather than continue.

Druckenmiller at Quantum first tried to short the tech stocks, but when he lost money on that, he pivoted to investing in them instead. When he felt the bubble was close to popping, he got out of the market, but then second-guessed himself one too many times and found himself owning tech stocks when the bubble finally did pop. Quantum’s losses were so significant Soros decided to stop speculating and convert his hedge fund into an endowment.

One of Mallaby’s main arguments for the utility of hedge funds is their tendency to push against market trends and toward market equilibrium, by shorting bubbles and buying in downturns. Neither of the big funds in 1999 seems to have taken that course. Perhaps their divine mandate turned against them when they forgot their true purpose.

VI. Third Generation Hedge Funds

Farallon

By the early 2000s, the three biggest hedge funds of the last half of the twentieth century had all closed up shop. Soros claimed it was the end of the age of hedge funds, but that is the sort of overdramatic megalomania one would expect from him, to believe just because he was done everyone else should be as well.

One of the most successful newer hedge funds was Farallon, started by Tom Steyer in 1985. Farallon was an “event-driven hedge fund”, which traded based off of “events” like mergers and bankruptcies. Stayer’s main strategy was betting on mergers. When a merger was announced, there was always uncertainty about whether it would go through, whether it would be stopped by anti-trust rulings, or whether something else would go wrong. Thus, the stock price between when a merger had been announced and when it was finalized was somewhere between the price if the merger didn’t go through, and the price if the merger did go through. The price only settled once there was certainty about the fate of the merger. By knowing more about anti-trust law, courts, and corporate procedures in general than the average investor, Stayer could make a good guess on the merger’s outcome. If he thought it would go through, he would buy the stock while it was still undervalued due to the uncertainty over the merger, and profit once the merger went through and the stock went up. And since Farallon was a hedge fund, he shorted the acquiring firms as a hedge.

Another trade he got into was junk bonds – bonds where the issuer is likely to go bankrupt and so the bonds have a high risk of not paying out. His superior understanding of bankruptcy law and knowledge about the issuing firms themselves meant he was better than the average investor at guessing whether the bonds would pay out or not, which meant he could pick out the junk bonds that were undervalued.

These strategies were very successful, and Farallon got into a partnership with Yale starting in 1990 to invest the money in their endowment, which started a trend as other universities invested in hedge funds as well. This was part of a larger shift where prior to the 2000s, hedge funds had mostly private investors. But in the 2000s, more of their investors were institutions. This came about as hedge funds became more mainstream and were seen as less risky. It helped that the new, event-driven hedge funds like Farallon, Perry Capital, and Och-Ziff had very little leverage, which meant they produced steadier returns. Though there was some pushback – for example, Farallon was protested by students when a controversial deal for developing an area of land got negatively covered in the media.

Medallion

The most successful hedge fund of the twenty-first century (at the time Mallaby’s book was published) was Medallion, founded by the mathematician James Simons in 1988. Simons initially tried the same sort of trend-following model that Steinhardt had used, but this had become too common among other funds and no longer brought profits. To paraphrase James Russell Lowell: “They must upward still, and onward, who would keep abreast of alpha-generating trading strategies.”

Part of Simons’s winning strategy was to recruit people from other fields – mainly mathematicians, but also computer scientists, physicists, astronomers – basically anyone except economists. This gave his fund’s associates an unusual perspective on markets. Or perhaps just unusual perspectives in general:

“On one occasion, a member of the faculty gave a presentation on how Medallion had performed over the past week; he presented Friday’s results first, followed by Monday’s, Thursday’s, Tuesday’s, and then Wednesday’s, assuming that his colleagues would find this bizarre sequencing natural, since computers sort days alphabetically.”

Medallion did not look at fundamentals, either of companies or the economy, but rather focused on very short-term trends in stocks, generally as short as a few days or less. By analyzing statistical patterns over data from thousands of trades, they made a mathematical model that could trade based on these short-term trends. Though the inefficiencies they were finding were very small, by discovering many of them and trading on them repeatedly, they made fantastic profits. Their edge was in finding trades where no one else was looking. Mallaby barely gives any details on these trades, which he openly admits is because he does not know any details to give. Medallion was run like a cult – very open internally, but secretive towards outsiders.

One of the people working for Simons, Elwyn Berlekamp, cashed out of the fund merely a year after it first made returns – massive 56% returns – to go back to doing research at Berkeley. In one way, this is surprising, considering Medallion’s future earnings. But I think the bigger surprise isn’t that some people cash out of funds that are on track to make billions, but rather that anyone persists through this millions-to-billions transition at all. After all, anyone whose fund is making millions could cash out and retire comfortably at any time. When they already have that much money, it’s not as if they’re improving their material quality of life by making more. But still, they choose to stay in the game. I think hedge fund people have to have a specific type of personality, one that doesn’t just tolerate risk but actively seeks and enjoys it: people with nerves of steel – people like George Soros, who even after losing $840 million in the 1987 crash, went right on trading for the rest of the year. Like Walter White, they’re not in it for the money. Neither do they trade in order to provide value to society or liquidity to markets, any more than Walter White was dealing drugs to provide a good life for Skylar. They’re in it for the love of the game itself.

Finance and drug dealing: both hobbies that can land you in prison, as Sam Bankman-Fried found out.

In 1993, Simons recruited Peter Brown and Robert Mercer who had also done work on statistical machine translation, which bore strong resemblances to Medallion’s method of quantitative trading. However, trading on trends that no one understands and that don’t make intuitive sense is dangerous, because there is potential to “recognize” a pattern that doesn’t actually exist. Also, there’s no way of knowing when the pattern might stop, making it impossible to get out ahead of the market. Nevertheless, the strategy was apparently very profitable for Medallion.

Mallaby also credits Medallion’s success to their culture, which was very different from the competitive multimanager structure of earlier funds like A.W. Jones’s or Tiger Management. In contrast, Medallion had group meetings every week where people presented their research findings and pitched ways they could improve their trading models, and people collaborated to figure out whether the ideas were worth incorporating.

Though Medallion was open on the inside, it was very secretive on the outside. This ended up benefitting it greatly during the market crashes of the later 2000s, when known trades had become crowded and stopped working when the hedge funds trading them started to liquidate. Meanwhile, Medallion’s trades that no one else knew about continued to work, as evidenced by Medallion’s continued profits. At one point, this secrecy was threatened when they unwisely recruited some Russians who tried to blackmail Simons into paying them more, threatening to take Medallion’s strategies to another fund. But Simons didn’t cave. The would-be blackmailers did go to another fund, but Simons sued them and ultimately made them stop trading. And even when they were trading, they still didn’t match up to Medallion’s performance.

A final factor in Medallion’s success was that it stayed small. By the 2000s, almost all the money in the fund was that of its own employees (though Simons started a bigger fund open to outside investors as well).

James Simons’s mansion in East Sestauket, NY. Also, where every millennial tells you they would be living if they had just been old enough and had capital to speculate with during the 2007 housing bubble.

Amaranth and Citadel

Not all hedge funds of the 2000s were destined to succeed; around this time, according to Mallaby, a hedge fund bubble was forming. One of the new multi-strategy funds was Amaranth, started by Nick Maounis in 2000. Amaranth’s strategy was varied – they did whatever worked at the time, dumping around half their capital into the strategy of the moment. To run all these strategies, Maounis hired various managers, including former Enron employees, while not understanding the strategies deeply himself. In short, he had no real edge over all the other funds like his being started around the same time.

Maounis’s biggest mistake, though, was hiring Brian Hunter to trade natural gas futures for him in 2004. While previously at Deutsche Bank, Hunter had also traded natural gas futures, betting on them staying low. This was such a bad call and resulted in such large losses that he had to leave Deutsche Bank. This time at Amaranth he was betting that natural gas futures would go up. The logic behind buying natural gas futures was that since gas shipped in pipelines and not in boats, supply couldn’t be quickly ramped up or down as it was needed. This made the prices volatile. And the reason it was seen as a good trade for speculators was that the options on natural gas were relatively cheap, so the traders stood to gain more than they stood to lose.

Natural gas futures might not have been a bad trade in principle, but in 2005, when Maounis was losing money on all his other strategies while the natural gas trade was profiting, he put 30% of his fund’s assets into it. This worked out in 2005 because of Hurricane Katrina, and they made $1.2 billion. But after hurricane season, Hunter continued to bet that the gas futures would rise on the logic that gas prices are always higher in winter than summer. He bet so strongly on this with such a large amount of Amaranth’s funds that he ended up holding more than half of some futures markets. And when gas futures did not behave as he had expected, he found himself trapped in the position, due to the large volume of his trades, as well as the fact that other funds were using this strategy as well, making the trades crowded.

When there was a rumor of more hurricanes coming the next year, Hunter decided to increase his positions. And when the hurricanes failed to materialize, the futures lost enough value they dragged Amaranth down to the point they got margin called and wound up in a crisis. Since other funds knew Amaranth had very big positions in these markets, people were expecting them to have to liquidate and traded against them. This created a vicious feedback loop, where Amaranth’s positions lost more and more. Maounis tried to get Goldman to buy part of his portfolio, but there was too much risk for Goldman’s taste since Maounis’s broker, Morgan Stanley, refused to agree to not clawback the money lent to Amaranth in the event of bankruptcy.

Ultimately, they found a buyer in the second biggest hedge fund of the era: Citadel, founded by Ken Griffin. Griffin had the advantage that he could make decisions quickly since his fund was more like a startup compared to the layered bureaucracy of Goldman. Also, Griffin’s people were very good at looking over other funds’ trades and books and figuring out what the value and risks of them were. In the end, Griffin and Morgan split Amaranth 50/50 in return for Morgan agreeing not to clawback their money. After Amaranth was bought by Citadel, the futures markets stopped being artificially distorted by speculators trading against Amaranth, since everyone knew Citadel had the capital to hold the futures Amaranth had bought and wouldn’t end up liquidating them in bankruptcy. The markets returned to normal, the futures regained their value, and Citadel profited $1 billion off of the buy, while Amaranth lost $6 billion of their investors’ money.

This near-disaster sparked suggestions that hedge funds should have to register with the SEC, since poor innocent pension plans were investing in them and they could wind up losing all their money. Mallaby thinks Citadel’s buying of Amaranth disproves this, and hedge funds can shoot their own rabid dogs. After all, according to Mallaby, hedge funds don’t get bailed out, or need help from the Fed – except for LTCM, which did need the Fed to come help them broker a deal, but apparently they don’t count.

VII. Mortgage-Backed Securities and Their Consequences

The 2007 Housing Bubble

Around 2005, many hedge funds started to realize there was a subprime mortgage bubble. The fact bad mortgages were being made wasn’t a secret, and funds started to position themselves for when it popped. However, in a world full of “unpredictable connections”, this was easier said than done.