On March 12, 2008, Fletcher Asset Management (a hedge fund management company run by Alphonse “Buddy” Fletcher) made a presentation to the Firefighters’ Retirement System of Louisiana, which was considering investing in one of Fletcher’s hedge funds. The presentation was impressive: one of Fletcher’s funds (Fletcher Income Arbitrage, Ltd.) reported annualized returns of 8.13% between June of 1997 and December of 2007, a period during which the fund had no down months. To sweeten the deal, FAM guaranteed returns of at least 12%, capped at 18%. If the pension plan’s investment returned less than 12%, the other investors would be subordinated to the pension plan to make up the difference (on the other hand, if the fund returned more than 18%, the surplus would accrue to the other investors).

You probably have a guess where this is going, and your guess is not wrong. In March of 2011, the Firefighters’ Retirement System and another Louisiana public pension plan asked for some of their money back.[1] Fletcher purported to satisfy the request by delivering promissory notes payable by one of the Fletcher hedge funds, due in June of 2013. Unsatisfied, the Louisiana pension funds made a full redemption request—they wanted all their money back.

But they didn’t get it. Facing an array of dilatory tactics, in January of 2012 the pension plans filed for the winding up of one of Fletcher’s funds in the Cayman Islands. In April a court approved the winding up. Copious litigation ensued. In June, one of FAM’s hedge funds, Fletcher International, Ltd., filed a chapter 11 bankruptcy case in the Southern District of New York, staying any litigation involving that fund.

In a chapter 11 case (unlike, say, a chapter 7 liquidation), the debtor’s existing managers generally keep their jobs. This is for at least two reasons. First, the idea of a reorganization is that the business will continue to operate, and existing management is deeply familiar with the debtor’s business. Second, it is thought that if existing management were immediately canned upon filing a bankruptcy petition, CEOs would not file a bankruptcy petition until too late to save the company. (That’s the way it worked under the previous bankruptcy statute, the Bankruptcy Act, which was thought to be unsatisfactory partly for this reason.)

Of course there are countervailing considerations, such as conflicts of interest and the basic fact that incumbent management presumably drove the company into insolvency in the first place. So the Bankruptcy Code allows a trustee to be appointed under chapter 11, and that’s what eventually happened with Fletcher International, Ltd. In September of 2012 Richard Davis, an experienced bankruptcy attorney with no previous involvement with Fletcher or his funds, was appointed as the chapter 11 trustee. His job was to maximize the value of the bankruptcy estate, pursue any claims it might have against insiders and third parties, and distribute the estate’s property to its creditors. He was also charged with drafting a report summarizing the events leading up to the bankruptcy case.

That report is the subject of this review. Here is a link to a PDF. Any information that I draw from outside the report will be accompanied by a link. Otherwise, everything comes from the report.

I should note at the outset that Davis, although not involved with the Fletcher companies prior to his appointment, was not a detached observer. In his role as trustee he was seeking to maximize the property available for distribution to creditors, and so he had reason to paint the estate’s legal claims (including claims against Buddy Fletcher) in a positive light. Also, much of what was written in the report consisted of allegations that have not been proven at trial. For simplicity I will not qualify his statements with “allegedly” or “according to Davis” throughout this review, but please note that I haven’t independently confirmed anything in his report, and you should take the facts describe below for what they are—allegations made in a court filing by a respected bankruptcy professional.

I will not try to give an exhaustive account of the report, but rather focus on one particular tactic used by Fletcher. This is partly because I think it sheds a lot of light on his practices, as well as the broader legal and financial world in which he operated, but also because, frankly, the report describes a bewildering tangle of entities and transactions that I still don’t fully understand after reading it twice.

Fletcher’s Investors

In all, during the events described here, FAM was managing initial investments of $125 million, $100 million of which came from the Louisiana pension plans (including the firefighters’ plan mentioned above) and $25 million of which came from the MBTA retirement fund.

Fletcher’s Compensation

This section describes how hedge fund managers are compensated. I’ve put one sentence in bold, which you should take note of, but otherwise if you already know how hedge fund compensation works then you can skip this section.

In general, compensation is divided into two components. One is a flat percentage of AUM, traditionally 2%. The other is called a “performance” or “incentive” fee, which is a percentage of the profits made by the fund. Traditionally this would be 20%, so that the manager would earn “two and twenty.” (In reality these fees are often negotiated and different investors may pay different fees. But for our purposes, this is good enough.)

Performance fees are calculated over specified periods of time, and subsequent losses don’t affect them. So for instance, let’s say I accept $100 million in investor money under a standard two-and-twenty compensation arrangement. In the first fee period, I earn trading profits of $40 million. In the second fee period, my luck runs out, and I lose $40 million in the markets. I close the fund and return investor money.

How much compensation did I earn? Let’s ignore AUM fees and focus on performance fees. Over the life of the fund, it was flat. But I will take home $8 million in performance fees, to reward me for the $40 million in profits I earned in the first fee period. Although I lost $40 million in the second fee period, I don’t have to pay back the $8 million or anything like that. And I certainly don’t have to pay 20% of losses.

By contrast, if I had gained and lost the $40 million within a fee period, the losses would offset the gains and I wouldn’t earn any performance fees. So the shorter the fee period, the more likely it is for the manager to earn performance fees based on transient gains.

The Davis report states that hedge funds typically calculate fees on an annual basis. But FAM calculated fees on a weekly basis. If Fletcher had one good week, then from a performance fee perspective it didn’t matter if the rest of the year was calamitous.

(There’s nuance here that I think we can mostly ignore. Compensation arrangements typically have a “high water mark” provision, where a fund manager isn’t compensated for performance that merely makes up previous losses. So for instance, if my fund went from $100 million to $140 million in the first calculation period, back to $100 million in the second, and then back to $140 million in the third, I would only earn performance fees in the first period. In the third period, I would be below my “high water mark” and so I wouldn’t be eligible for performance fees.)

Cashless Exercise

Let’s focus on one particular aspect of FAM’s practices. Fletcher invested much of his investors’ money in PIPEs – private investments in public equity. These are not inherently sleazy. Davis notes in the report that Warren Buffett famously made an investment in Goldman Sachs through a PIPE. PIPEs are also commonly used in connection with SPACs (if you don’t know what that is, don’t worry about it).

Normally if you want stock issued by a publicly traded company, you simply buy it on the stock exchange. You don’t know or care who sold you the securities, and you don’t negotiate the price. In a PIPE, by contrast, you don’t buy the shares from an anonymous seller, you buy them directly from the company. The company often sweetens the deal by giving the buyer warrants on its stock. (A warrant is just the name given to a call option that is written by the company itself, not by a third party. I’ll use the terms “warrant” and “option” interchangeably.) PIPEs are heavily negotiated and they can be particularly attractive for distressed companies that need infusions of cash.

PIPEs don’t have to be particularly hard to value. But as we’ll see, Fletcher’s PIPEs were not only difficult to value, they were impossible to value without resolving difficult legal questions. To understand why, we have to look at the warrants that Fletcher’s funds received in the PIPEs.

Remember that a warrant is just a call option. It is the right, but not the obligation, to buy a specified number of shares for a specified price in the future. If I have a warrant to buy 100 shares of stock for $20 per share, then I can exercise it by paying $2,000 to the issuer of the shares. Of course I will only exercise the warrant if the shares are worth more to me than the strike price. If not, I will just let the warrant expire.

In practice, the holder of a warrant will often sell the shares immediately upon exercising the option, realizing a profit on the difference between the strike price and the market price of the shares. One usually minor issue is that the investor has to come up with the cash to pay the strike price. This is a very temporary problem—the holder of the warrant can just sell the shares to recoup the strike price. (If the shares aren’t worth enough to pay the strike price, then the holder simply won’t exercise the warrant.) Still, although it’s pretty minor, this annoyance can be avoided entirely with what is called “cashless exercise.”

In cashless exercise, the holder of the warrant doesn’t pay any cash, and the company delivers a smaller number of shares than it otherwise would. In essence the parties net down the obligations so that the company simply delivers shares with a value equal to the profit the investor would have made under traditional exercise. Of course the warrant holder can still sell the shares immediately (and often would), but it’s no longer necessary to do so to recoup the strike price.

So it’s common to include a contractual provision allowing for cashless exercise. The way it works is that you calculate the inherent value of the option, which is simply the market value of the shares minus the strike price, times the number of shares. So if you have the right to buy 100 shares for $10, and you can sell them on the market for $20/share, then at the time of exercise your option is worth $1,000 ($20/share minus $10/share, multiplied by 100 shares). To translate this into a number of shares, you divide $1,000 by $20, which is the price of a share. So under cashless exercise, you would get 50 shares.

The math checks out: 50 shares are worth $1,000 on the market, which is exactly what you would have netted if you had bought all 100 shares for $10 each and then sold them for $20. So in a traditional exercise you pay $1,000 for 100 shares (worth $2,000 at current market prices), and in cashless exercise you pay $0 for 50 shares (worth $1,000 at current market prices). It’s the same profit either way, but cashless exercise has the advantage that you don’t have to come up with $1,000.

Fletcher’s PIPE agreements provided for cashless exercise, with the number of shares to be delivered by the issuer determined according to the following formula:

X = N(S-K)/K

where:

X = the number of shares of stock to be issued pursuant to the cashless exercise provision

N = the number of shares of stock for which this warrant is being exercised without a cashless exercise provision

S = price per share of the stock

K = the exercise price for the stock

Pause here and imagine that you are a lawyer representing a company that is negotiating a PIPE with Fletcher. You’ve come to the cashless exercise section of the contract, and you see the formula above. What do you make of it? Remember, Fletcher invested mostly in distressed companies, so don’t spend too long thinking about it. Your client can’t afford big legal bills.

Did you spot the problem? Here’s the standard formula for cashless exercise:

X = N(S-K)/S

See the S in the denominator? You’re supposed to divide the inherent value of the option by the market value of the shares. In Fletcher’s formula, you divide the inherent value of the option by the strike price. So according to his formula, in our fact pattern you would divide $1,000 by $10, and you would be entitled to 100 shares in a cashless exercise. That’s the same number of shares you would get if you paid the strike price in cash! Cashless exercise would net you a $2,000 profit, which is double what your option is supposed to be worth under these parameters.

And it gets worse the higher the market price goes. If the strike price on a 100-share warrant is $10 and the shares are worth $50, the traditional cashless formula would give you 80 shares, for a profit of $4,000 (as expected). But Fletcher’s formula would give you 400 shares, for a profit of $20,000! Simply by choosing a cashless exercise, you would quintuple your profits relative to traditional exercise. (You would also get 4 times as many shares, a completely perverse result. The whole point of cashless exercise is to accept fewer shares in return for the company waiving the payment of the strike price.)

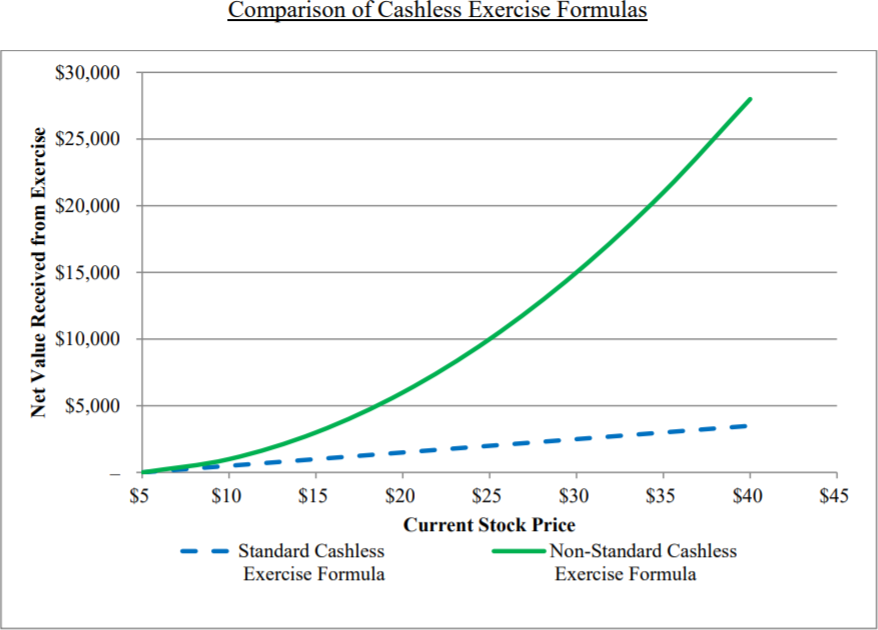

If Fletcher’s formula is taken literally, his warrants had incredible latent value, much of which would be realized only if the underlying stock appreciated by a lot. Remember, these issuers tended to be financially distressed, so you might not expect their stock to perform very well. Still, when a stock has an uncertain future value, an option with those characteristics would be very valuable. The Davis report provides a helpful graph illustrating how the Fletcher formula boosts returns relative to the standard formula (see page 185):

If you didn’t spot the problem with Fletcher’s formula, don’t feel too bad. Although he used the non-standard formula for PIPE agreements with several companies, none of them came to grief. One company noticed the flawed formula after signing the agreement, and when it complained, Fletcher agreed to amend the contract to use the standard formula. In another case a Fletcher fund successfully used his formula to exercise a warrant, but the strike price was so close to the market price that it made little practical difference. (See the graph above. At low values, the lines are pretty close together.)

But if Fletcher never used the formula to squeeze much money out of the companies he invested in, then what was the point?

The following bullet points are quoted directly from pages 16 and 17 of the Davis report (“FILB” is short for Fletcher International, Ltd. – the B stands for “Bermuda,” and “ANTS” is ANTS Software Inc.):

- On March 15, 2010, FILB invested $1.5 million in ANTS, receiving common stock (then trading at 90 cents) and warrants to purchase another 10 million shares.

- On March 31, 2010, FAM marked up this investment, despite there having been no fundamental change at ANTS, to $17.3 million (a 1,053% gain in 16 days) even though at the same time the ANTS 2009 audited financials were released, raising “going concern” issues (a fact FAM neglected to mention in highly optimistic reports to the MBTA Pension Fund).

- FILB, either directly or through BRG (a FILB subsidiary), invested an additional $5.9 million in ANTS during 2010, and at its high point, FAM marked the investment at $62.8 million.

- Ultimately, FILB recovered $4.9 million of the $7.4 million it invested; the remaining warrants are worthless.

- Nevertheless, on an investment where FILB lost $2.5 million (ANTS), FAM took management and incentive fees as if it were worth 1,164% more than the investment actually returned.

Here are some more examples, again quoting directly from the Davis report (pages 179-80):

- On December 31, 2010, FILB made a $4 million investment in DSS. On the same day, FAM marked that position at $23.6 million, suggesting an immediate unrealized profit of $19.6 million.

- On February 25, 2011, FILB made an investment in a warrant issued by HPG that had been acquired for $1 million. By February 28, 2011 – the next business day – FAM had marked the position at $25.7 million. This effectively meant that for $1 million spent by FILB, FAM received credit for $24.7 million in earnings, which on the margin would result in an approximate $5 million fee.

And here’s the aggregate math (directly quoting from page 179 of the report – citations omitted):

Between 2007 and the bankruptcy filing in June 2012, FILB initiated ten new PIPEs or warrant investments. The ten investments were marked as of the month-end immediately following the investment at a cost-weighted average multiple of 2.7 times what FILB had just paid for them. In other words, if FILB invested $10 million, on average the month-end initial mark for the investment would have been $27 million, thus presenting a likely fictitious (and unrealized) profit of $17 million. FAM would base its fees on this fictitious mark, and it would report AUM and returns on investment based on that mark.

I should note that the cashless exercise formula probably wasn’t the only way Fletcher inflated these valuations. As Davis documents, Fletcher’s valuation agent had significant undisclosed conflicts of interest— for instance, it wanted to start its own hedge fund management business, and Fletcher was in talks to provide the seed capital. But the formula certainly helped the valuation agent give Fletcher the numbers he wanted. Simply by assuming the formula was enforceable as written, the agent could massively inflate the values of the warrants.

An Academic Interlude

It’s worth stopping to ask why or whether this was a bad assumption. Sure, the valuations may look ridiculous in retrospect, but if a few of these companies had turned out to be big winners, then wouldn’t the valuations have been justified? I refer you again to the graph I’ve reproduced above. At low values, Fletcher’s formula doesn’t do much. But at high values, it yields insane rates of return. Why was it wrong to take those potential home runs into account, even if in retrospect we know the companies mostly faltered?

The problem with attributing these values to the warrants is that it implicitly assumes that the warrants were enforceable according to their literal terms. You can probably get into a long argument with a New York lawyer about this if you want. In general, New York law favors freedom of contract. Of course there are a lot of exceptions, but few of them would apply to a commercial contract signed by sophisticated parties, each represented by capable lawyers. Courts will rectify obvious typos, but for a court to second-guess a financial formula would be fairly rare. If the parties want to use a weird formula, they can do it.

But that’s a big if. The more natural interpretation, in a case like this, is that there was a typo, what the courts sometimes call a “scrivener’s error.” Courts don’t want to interpret language mechanically when it would yield barbarous results. Imagine a divorce settlement in which the parent who is granted custody undertakes to raise the child in “New York, Connecticut, or Jersey.” Given the context, a court is likely to interpret that to mean New Jersey, not the channel island with a similar name.

If the parties really do want to allow the parent to raise the kid on the isle of Jersey, they can certainly accomplish that. They just need to make it clear to the court that this is what they mean. “Custodial parent shall make best efforts to raise the child in the State of New York, the State of Connecticut, or the Bailiwick of Jersey, located in the English Channel.” No ambiguity there.

The problem for Fletcher is that if he spelled out the effect of his formula in plain, unambiguous English, opposing counsel would probably catch it. And having caught it, they might realize he’s a scumbag and raise a big stink, scuttling his entire enterprise. He had to slip it in as a plausible typo, and the cost of doing that is that you really don’t get anything approaching legal certainty that way. Of course, as discussed above, Fletcher didn’t need legal certainty, he just needed a fig leaf for his valuation agent.

It’s telling that in the one case a company noticed the erroneous formula, Fletcher gave up without a fight. In that case, while the Fletcher formula was in the contract, he valued the warrants at $76.3 million. After amending the contract to replace it with the standard formula, he reduced the valuation of the warrants to $14.9 million, wiping out $61.4 million in value. Giving up that much putative value without a fight is not consistent with the formula being bulletproof in court.

Taking Stock

To my knowledge, Fletcher has not been charged with any crime. This is despite the unbelievable behavior described in the Davis report and the incredible fact that, as far as I can tell, Fletcher’s investors would have done better, financially, if they had invested their money with Bernie Madoff.

Not that Fletcher escaped completely unscathed. He did lose his business. He sold his Connecticut castle at what seems like a fire sale price. After 10 years of marriage, his wife, Ellen Pao, found that the spark had gone—she is divorcing him and invoking their prenuptial agreement to keep his hands off her wealth. Her lawyer said Fletcher is known in the media as a “disgraced hedge fund manager.”

But disgrace is in the eye of the beholder. Harvard University has many professors, but at the time I am writing this review, the title of “University Professor” is reserved for 26 superbly accomplished academics. Among them is Henry Louis Gates, Jr., who has the honor of serving as the Alphonse Fletcher University Professor. Gates described his appointment as “without a doubt the greatest honor of my academic career.”

On the other hand, Gates is also presumably a user of the MBTA system, or at least pays taxes to support its retirement fund, which just shows that you can’t win them all.

Footnotes

- ↩

As a side note, it appears that the source of the pension plans’ concern was a public allegation by the coop board of the Dakota, a famous building in New York, that Alphonse Fletcher was exaggerating his company’s “assets under management.” AUM is the total amount of investor money that a fund manager controls, and as we’ll see the manager’s compensation is partly a function of AUM. Fletcher had sued the board, arguing that he was denied the right to buy another unit in the building due to racism (Fletcher is black). The board responded, in essence, we’re obviously not racist since we already let you buy several units in the building. We just don’t think you can afford the upkeep.

If you only learn one thing from this review, let it be this: never, under any circumstances, get in a public fight with your coop board.